Health insurance for parents protects their access to quality medical care without depleting retirement savings. Dedicated policies or family floaters cover critical illnesses, pre-existing conditions, and hospitalization. You can secure these plans through tailored senior citizen packages or add them to your own comprehensive plans. Choosing the right one depends on your parents' age, health profile, and budget.

Ditto rates plans using policy features, insurer metrics, and premium value. Based on this, Ditto's top pick is Optima Secure, backed by HDFC Ergo's 96.71% average claim settlement ratio (FY 2022-25). For reference, a family floater for two parents aged 60 and 62 costs around ₹79,369 per year for a ₹15 lakh cover.

This guide is for anyone buying health insurance for aging parents, whether they are in their 50s or already above 60.

Your parent needs a knee replacement or a cardiac procedure. The hospital bill comes to ₹4 lakh-₹6 lakh. Your savings take a hit, and your family spends months recovering financially.

This is exactly what health insurance for parents is meant to prevent. But not all plans are built the same. Many plans aimed at older age groups come with copays, room rent caps, and sub-limits that quietly eat into your coverage when you actually need it.

In this guide, we will discuss why your parents need their own health policy. We’ll also compare the best health insurance plans for parents in India, types of health insurance plans, key features to look for, and premiums.

Confused about which plan to take for your parents? Book a call or WhatsApp us for clarity.

Why Your Parents Need Their Own Health Insurance Policy

Healthcare Costs Are Rising

Medical inflation in India is running at 12.9%-14% annually. A single hospitalization can cost more than you expect. Without insurance, one medical emergency can wipe out years of savings.

Buying Early Gives Better Access

Insurers are likely to approve applications when your parents are relatively healthy. Pre-existing disease (PED) waiting periods start from the policy's inception, so the earlier you buy, the sooner you will be covered.

Aging Brings More Health Issues

According to a Press Information Bureau (PIB) report, India's elderly population is projected to reach 230 million by 2036. As parents age, hospital visits, tests, and follow-ups become more frequent, and the right policy ensures these costs do not drain your savings.

Coverage for Extra Expenses

Most comprehensive plans cover hospitalization-linked pre- and post-hospitalization expenses and annual health check-ups. Outpatient Department (OPD) consultations, pharmacy bills, and diagnostics may be covered only if the plan has an inbuilt OPD benefit or if you buy an add-on.

Best Health Insurance for Parents in India

01

HDFC ERGO

Optima Secure

HDFC Ergo is one of the most trusted health insurers in India. It has a 96.71% average claim settlement ratio (FY 2022-25), a network of 13,000+ hospitals, and one of the lowest complaint volumes in the industry at just 9.28 per 10,000 claims.

HDFC ERGO

Optima Secure

4.6

Overall Rating

Insurer Rating

5.0/5

Customer Service

5.0/5

Features

4.6/5

Premium Rating

3.0/5

Key Features

Secure Benefit doubles your cover from day 1, so a ₹15 lakh plan immediately gives you ₹30 lakh in coverage.

Plus Benefit boosts your base cover by 50% up to 100% of the sum insured (SI), even if you have made claims.

Restore Benefit refills 100% of the base sum insured for later claims in the same year, and can be made unlimited via an add-on.

Protect Benefit covers non-medical consumables like gloves and masks by default, which cuts out-of-pocket costs during claims.

ABCD Chronic Care add-on reduces the waiting period for pre-existing Asthma, Blood Pressure (BP), Cholesterol, and Type 2 diabetes from 3 years to just 30 days.

Watch Out For

Premiums are on the higher side. Underwriting can be stricter, too, so parents with a significant medical history may face premium loading or rejections in some cases. The ABCD Chronic Care add-on must be paid for each year and cannot be dropped mid-policy.

A Note on Optima Secure+

If your parents are below 60, consider Optima Secure+ instead. It is built on the same strong foundation as Optima Secure. But it offers a few additional benefits, such as an in-built unlimited restoration benefit and 100% of SI as a bonus, with no upper cap on accumulation. This gives younger parents more room to grow their coverage over time. The insurer, core features, and claim experience remain the same.

Ditto's Verdict

If your parents clear underwriting and the premium fits your budget, Optima Secure is the strongest comprehensive plan available.

2

Care Health

Care Supreme

Care Health has an average claim settlement ratio of 93.13% (FY 2022-25) and a network of 11,400+ hospitals. The complaint volume is at 42 complaints per 10,000 claims.

Care Health

Care Supreme

4.5

Overall Rating

Insurer Rating

4.2/5

Customer Service

3.0/5

Features

4.5/5

Premium Rating

5.0/5

Key Features

Unlimited Automatic Recharge refills the cover an unlimited number of times in the same year, even for the same illness.

The inbuilt cumulative bonus increases the cover by 50% per year, up to 100%, and does not reduce even after a claim.

The Cumulative Bonus Super add-on adds another 100% per year up to 500% on top of the inbuilt bonus, and the Cumulative Bonus Booster offers 100% bonus per year with no upper capping on accumulation.

Instant Cover add-ons reduce the waiting period for pre-existing ailments such as asthma, diabetes, and hypertension from 3 years to 30 days.

PED waiting reduction add-on shortens the pre-existing disease wait from 3 years to 1 or 2 years.

Watch Out For

Consumables coverage and health check-ups are optional add-ons and cost extra. Complaint volume is also higher than that of some peers, so the service consistency can vary.

Ditto's Verdict

If you want a well-priced plan for parents with strong inbuilt recharge and flexible add-ons to reduce waiting periods, Care Supreme is a solid choice. Another benefit is that the PED reductions add-ons can be removed after 3 years, so you don’t have to bear the extra costs later. It is particularly useful if you want an insurer that does not apply loading charges in most cases.

3

Aditya Birla

Activ One Max

Aditya Birla has an average claim settlement ratio of 95.81% (FY 2022-25) and a network of 12,000+ hospitals. The complaint number is decent, with just 18.66 complaints per 10,000 claims.

Aditya Birla

Activ One Max

4.4

Overall Rating

Insurer Rating

4.5/5

Customer Service

5.0/5

Features

4.3/5

Premium Rating

5.0/5

Key Features

Super Reload refills the cover an unlimited number of times if there are multiple claims in the same year.

Super Credit bonus increases the cover by 100% of the base sum insured at each renewal, up to 500% and capped at ₹3 crore, regardless of claims made.

Claim Protect covers non-payable items by default, reducing common out-of-pocket costs at the time of claim.

Chronic Care add-on provides day 1 coverage for specified chronic conditions, such as diabetes and hypertension.

HealthReturns can refund up to 100% of the renewal premium based on your fitness activity and health metrics.

Watch Out For

Aditya Birla is a comparatively newer insurer, and some parents may prefer a more established name. PED reduction and chronic care add-ons need to be paid for every year and cannot be dropped mid-policy.

Ditto's Verdict

If you want comprehensive cover at an affordable premium with lenient underwriting, Activ One MAX is a strong fit and a good option for parents who may not get approved easily under stricter insurers.

4

Niva Bupa

ReAssure 2.0 Platinum+

Niva Bupa has a 91.62% average claim settlement ratio (FY 2022-25) and a network of 10,000+ hospitals.

Niva Bupa

ReAssure 2.0 Platinum+

4.3

Overall Rating

Insurer Rating

4.2/5

Customer Service

3.0/5

Features

4.2/5

Premium Rating

5.0/5

Key Features

ReAssure Forever triggers unlimited refills for life after the first paid claim, so future claims can always go up to your full SI.

Booster+ carries forward unused base sum insured and can build it up to 5x over time.

Lock the Clock locks your premium to your entry age until a claim is paid, though insurer-wide repricing and medical inflation can still affect it.

Disease Management Rider add-on provides immediate cover for hospitalization due to complications from diabetes or hypertension.

Safeguard/Safeguard+ add-on covers non-payable items, protects booster+, and increases cover with inflation, reducing out-of-pocket costs at the time of a hospital bill.

Watch Out For

Complaint volume is higher than that of some peers, at 42.85 per 10,000 claims, indicating the service experience can vary.

Ditto's Verdict

If you want an innovative plan structure and are comfortable doing a careful check of the policy terms, Niva Bupa ReAssure 2.0 Platinum+ is a decent option for parents.

5

SBI General

Super Health Platinum Infinite

SBI General has a 96.14% average claim settlement ratio (FY 2022-25) and the largest hospital network on this list at 16,600+ hospitals. The complaint volume is at 20.51 complaints per 10,000 claims.

SBI General

Super Health Platinum Infinite

4.1

Overall Rating

Insurer Rating

3.8/5

Customer Service

3.0/5

Features

4.2/5

Premium Rating

5.0/5

Key Features

Reinsure Benefit provides unlimited restoration in the same policy year from the first paid claim, up to 200% of the base sum insured.

Health Multiplier increases coverage by up to 3x for 37 listed serious illnesses, such as cancer and kidney failure.

Claims Shield covers consumables like gloves, masks, cotton, and bandages, reducing out-of-pocket costs.

Pre-existing diseases are covered after just 2 years, which is shorter than most plans on this list.

Watch Out For

This plan starts at a ₹50 lakh sum insured, so it sits at the premium end of the market. Servicing can be more process-heavy, which may mean slower grievance resolution.

Ditto's Verdict

If you want strong restoration, a shorter PED waiting period, and high coverage, SBI Super Health Platinum Infinite is worth shortlisting. Just be prepared for a more formal service experience.

Note: If you'd like to explore the detailed figures reported by insurers and the IRDAI in their annual disclosures and public reports, visit Ditto Data Labs, our proprietary repository of health insurance data, meticulously compiled, verified, and maintained by the Ditto team over the years.

Types of Health Insurance Plans for Parents

Family Floater

You buy one floater and include yourself, spouse, kids, and parents under the same sum insured.

When It Can Make Sense

When your parents are relatively young and healthy, think late 40s or early 50s.

You want the simplicity of managing one policy.

The Catch

Most insurers cap floaters at 2 adults, so adding both parents in addition to yourself and your spouse is possible, but rare, like in HDFC Optima Secure, we can add 4 adults in the same plan.

Your parents' ages largely drive your premium, since the oldest member sets the price.

One large claim by any member eats into the shared cover for everyone.

Separate Policy for Parents

This means either one floater for both parents or individual policies for each.

Which Works Better

A floater for both parents is usually cheaper, and restoration plus bonus features make the shared cover sufficient for most situations.

Individual plans make sense if your parents have very different health profiles or qualify for different plans.

Why Is This Recommended

Your parents' premium stays completely separate from your own plan.

Their claims do not affect coverage available to your spouse or kids.

You can pick features built for older ages, like shorter waiting periods, home care, or OPD coverage, without making trade-offs on your own plan.

Your parents cannot get a comprehensive plan due to underwriting restrictions.

The Catch

These plans often carry copayments, room rent limits, and disease-wise sub-limits.

Premiums may look lower upfront, but out-of-pocket costs during claims tend to be higher.

Base Plan + Super Top-Up

A base policy combined with a super top-up to extend coverage at a lower overall cost.

When It Can Make Sense

You want higher overall coverage without paying for a high-sum-insured base plan.

Underwriting limits how much base coverage your parent can get.

The Catch

The super top-up only activates after cumulative claims cross the deductible threshold for the year.

Underwriting can be strict here, too, so approval is not guaranteed.

If the base plan and super top-up are from different insurers, getting cashless coverage for both simultaneously can be complicated.

Corporate or Employer Health Insurance

Many employer group policies offer easier access and may cover parents without individual medical underwriting, but the benefits depend entirely on the employer’s policy. Check whether parents are covered, if PEDs are covered from day one, the sum insured, copay, room rent limits, disease sub-limits, and whether you have the option to continue the cover if you change jobs.

Treat this as a bonus layer, not your primary plan. Coverage can disappear if you switch jobs, retire, or your employer revises the policy. That said, there are situations like rejection from all retail plans, where it becomes the only option.

Talk to an expert today and find the right insurance for you.

Should You Include Parents in a Family Floater or Buy Separate Plans?

Feature

Family Floater

Separate Plan

Premium

Lower overall, but rises steeply when older parents are included

Higher, but predictable and independent

Claim Impact

One large claim can exhaust the cover for all members

Your cover is not affected by your parents' claims

Sum Insured

Shared among all members

Dedicated to parents alone

Flexibility

Less flexibility if parents need specialized cover

Can be customized specifically for parents

Takeaway: Buying a separate plan is almost always the better choice. Their higher risk profile will significantly increase the premium for the entire family floater. And if one parent has a major hospitalization, the shared coverage may not be enough for the rest of the family.

Key Features to Look for When Buying Health Insurance for Parents

01

No Restrictions

The first thing to check is whether the plan has copayments, room rent limits, or disease-wise sub-limits. These three are the most common reasons claim payouts get reduced, and they hurt more at older ages when hospital bills are larger. Even a ₹25 lakh cover with a 20% copay and a room rent cap can feel like much less when the bill actually arrives.

02

Waiting Periods and Add-Ons

Most parents have at least one pre-existing condition. Plans cover these only after a waiting period, typically 2-3 years. Many insurers offer paid add-ons to shorten this, but check two things before assuming it helps. First, confirm your parent's specific condition is included in the add-on. Second, check whether the add-on must be paid every year to keep the reduced waiting period active.

03

Restoration Benefit

If a parent exhausts the sum insured in one hospitalization, restoration refills the cover for future claims in the same year. This matters more for older parents who may have multiple hospitalizations in a single year. Check whether restoration applies to the same illness or only unrelated ones, and whether it can be upgraded to unlimited times via an add-on. Also, check whether it works on partial or complete exhaustion of the sum insured.

04

Bonus

A good cumulative bonus increases the sum insured each year, regardless of claims. Over time, this can significantly increase the effective cover without additional premium. More importantly, check whether the bonus drops after a claim. Some plans protect it, others reset it entirely.

05

Adequate Sum Insured

A high base sum insured can be expensive or hard to get approved at older ages. A practical approach is to aim for ₹15 lakh-₹25 lakh as the base if underwriting allows. If only a lower sum insured is available, layer it with a super top-up to extend coverage at a lower additional cost.

06

Cashless Hospital Network

Check that the insurer has a strong cashless network in your parents' city, specifically, not just nationally. A wide overall network means little if the good hospitals near your parents are not empaneled. Also, confirm how smooth the cashless process is in practice by inquiring with the hospital.

07

Service Quality

Claim settlement ratios across good insurers look similar on paper. The real difference shows up during a claim. Look at complaint volumes, how smooth cashless approvals are in your parents' city, and how process-heavy the insurer is known to be. For parents, a smoother claim experience often matters just as much as the policy terms themselves.

Health Insurance for Parents Above 60: What Changes?

Premiums Increase Significantly: This is the most immediate change. Premiums for a 60-year-old can be 3-4 times higher than what a 35-year-old pays for the same cover. And they continue to rise with renewals as age increases. Budgeting for this early, ideally by buying before 60, makes a meaningful difference. You can also check our guide on tips to reduce health insurance premiums.

Underwriting Gets Stricter: Insurers will almost always require pre-policy medical tests before issuing a policy after age 60. Conditions like diabetes, hypertension, or a history of cardiac issues can lead to premium loading, permanent exclusions for specific illnesses, or outright rejection.

Your Options Narrow: Above 60, insurers become more selective. Some plans may not be available at all beyond a certain entry age. The ones that are available may come with more restrictions, or the premium may be high enough that senior-citizen-specific plans start to look like the only practical option.

Waiting Periods: If your parent is buying a new policy with a known condition, that condition will not be covered for the first 2-3 years unless a waiting period reduction add-on is available and covers that specific illness. There is a 2- year mandatory waiting period for specific conditions like cataract, hernia, etc. This is one more reason to buy early.

How Much Sum Insured Is Right for Your Parents?

There is no one-size-fits-all sum insured. However, considering rising medical inflation and a long-term perspective, we recommend a cover of ₹15 lakh-₹25 lakh.

Here's a practical starting point:

Parents Below 60, Metro City: Minimum ₹15 lakh-₹25 lakh.

Parents Above 60, Metro City: Minimum ₹20 lakh-₹25 lakh.

Parents With a History of Cardiac Issues, Diabetes, Bone Issues, or Asthma: Consider ₹25 lakh and above.

Premium Costs for Parents' Health Insurance: What to Expect

Profiles

HDFC ERGO Optima Secure/ Optima Secure+

Care Supreme

Aditya Birla Activ One MAX

Niva Bupa Reassure 2.0 Platinum +

Family Floater, 2A: Ages (50, 52)

₹45,726 / ₹45,985

₹51,973

₹39,398

₹44,140

Family Floater, 2A: Ages (60, 62)

₹79,369 / NA

₹86,069

₹66,505

₹75,171

Family Floater, 2A: Ages (65, 67)

₹1,08,602 / NA

₹1,17,720

₹87,805

₹98,897

Note: Here ‘A’ stands for adult. Premiums are for a ₹15 lakh SI, residing in Delhi - 110010, including necessary and mandatory add-ons. Exact premiums can vary depending on city, underwriting, discounts, and age.

The IRDAI 10% Annual Premium Cap for Senior Citizen Plans

In January 2025, IRDAI issued a directive that directly protects senior citizens from sudden, steep premium hikes. The rule is straightforward.

Insurers can revise health insurance premiums for senior citizens (60+) by no more than 10% per year without prior consultation with IRDAI.

If an insurer wants to revise premiums by more than 10% in a given year, it must first obtain regulatory consultation.

Insurers also need IRDAI's permission before withdrawing any health insurance plan specifically designed for senior citizens.

This came after years of seniors experiencing renewal shocks, with premiums sometimes doubling in a single year.

What to Do If Parents Cannot Get Health Insurance?

Sometimes, a parent's medical history, such as a history of cancer, a cardiac event, or multiple chronic conditions, makes it very difficult to get a regular retail health insurance policy. In such cases, here is what you can do.

Option 1: Government Schemes

The Pradhan Mantri Jan Arogya Yojana (PMJAY) covers up to ₹5 lakh per family per year for eligible households. Some states have their own state health schemes on top of this. The government expanded Ayushman Bharat PM-JAY in September 2024 to cover all senior citizens aged 70 and above, regardless of income. Eligible seniors receive up to ₹5 lakh per year for secondary and tertiary hospitalization at empaneled public and private hospitals.

Option 2: Senior Citizen Specific Plans

Some insurers specialize in covering older individuals with pre-existing conditions. Plans like Care Senior Health Advantage and Star Senior Citizen Red Carpet may be worth exploring. They tend to carry copayments, but they do provide a meaningful safety net.

Option 3: Your Corporate Group Cover

Shrehith, one of Ditto's co-founders, uses his corporate group cover primarily for his father. His father's medical history makes it very difficult to get a regular retail health insurance policy. In such cases, a corporate group health policy can be the only practical safety net. It provides coverage regardless of medical history, because group plans cover everyone without individual underwriting.

So yes, try to buy a personal health insurance plan for your parents early if you can. But if a parent is no longer eligible for retail coverage, your corporate group coverage can still play a very important role.

Tax Benefits When Buying Health Insurance for Parents

Under Section 80D (now Section 126) of the Income Tax Act (old tax regime), you can claim deductions as follows:

Who Is Covered

Deduction Limit

Self, spouse, and children (below 60 years)

Up to ₹25,000 per year

Self, spouse, and children (self/spouse above 60)

Up to ₹50,000 per year

Parents below 60 years

Additional ₹25,000 per year

Parents above 60 years (senior citizens)

Additional ₹50,000 per year

Maximum possible deduction

Up to ₹1,00,000 per year

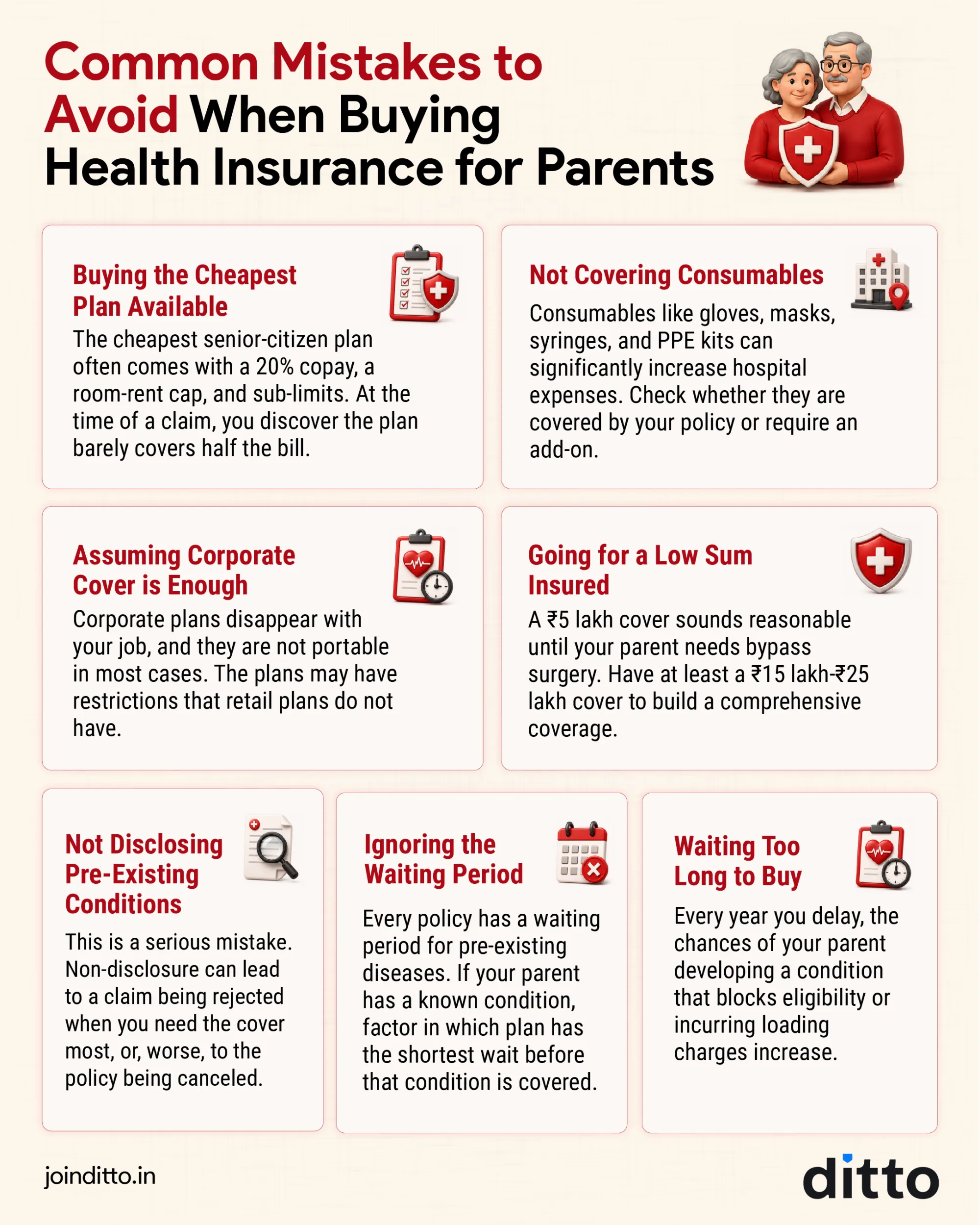

Common Mistakes to Avoid When Buying Health Insurance for Parents

Have a look at the infographic below to understand the common mistakes and how to avoid them:

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 24,000+ happy customers

Buying health insurance for parents is not just about picking a plan. It is about ensuring the plan actually pays out when it matters. The real regret is never about paying a slightly higher premium. It is discovering at claim time that a copay, room rent limit, or sub-limit has quietly reduced what you actually receive.

Here is a simple way to approach it:

Start with the structure. A separate policy for parents is almost always the cleanest option. Their claims stay independent and do not affect your family's cover.

Shortlist 2-3 plans and read the fine print. Focus on PED waiting periods, copay clauses, and any restrictions that reduce payouts. Do not just compare premiums.

Disclose everything during the application. Judge the plan only after you see the final underwriting terms, not the brochure premium.

If the base cover feels expensive, do not force it. Buy the best base plan you can sustain, then layer a super top-up for bigger hospital bills.

The goal is a plan that holds up when your parents actually need it, not just one that looks good on paper today.

Disclaimer

We believe in full transparency around our partnerships. Our current insurer partners are HDFC Ergo, Care, Aditya Birla, and Niva Bupa. But as you can see in this list, the rankings include both partners and non-partners because the methodology is unbiased and applied uniformly across all insurers.

Frequently Asked Questions

Should I add my parents to my family floater or buy them a separate health insurance plan?

Buying a separate health insurance plan for parents is almost always the better choice. When you add older parents to a family floater, the premium for the entire policy rises sharply because the oldest member determines the price. One large claim by a parent can also exhaust the shared cover, leaving nothing for your spouse or kids. A separate plan keeps their coverage independent, lets you pick features built for older ages, and ensures their claims never affect your family's protection.

What is health insurance for parents above 60, and what should I look for?

Health insurance for parents above 60 covers hospitalization, surgeries, pre- and post-hospitalization costs, and often OPD consultations for senior citizens. When buying, look for plans with no copay, no room rent limits, and no disease-wise sub-limits, since these restrictions reduce payouts significantly at older ages. Check waiting periods for pre-existing diseases, restoration benefits, and the insurer's cashless network in your parents' city. Premiums for a 60-year-old can be 3 to 4 times higher than what a 35-year-old pays for the same cover.

Can I get health insurance for parents with pre-existing conditions like diabetes or hypertension?

Yes, most comprehensive health insurance plans for parents cover pre-existing conditions after a waiting period of 2 to 3 years. Many top plans also offer paid add-ons to shorten this wait. For example, HDFC Ergo Optima Secure's ABCD Chronic Care add-on reduces the waiting period for Asthma, BP, Cholesterol, and Type 2 diabetes from 3 years to just 30 days. Always confirm that your parents' specific condition is listed in the add-on, and check whether it must be paid annually to keep the reduced waiting period active.

What is a super top-up plan, and should I use it for my parents?

A super top-up plan activates once cumulative claims in a year cross a set deductible threshold. It is a cost-effective way to extend total coverage without paying for a high sum insured base plan. For parents who cannot get approved for a high base cover due to underwriting restrictions, pairing a lower base plan with a super top-up may be a practical approach. At Ditto, we recommend making sure the base plan and top-up are from the same insurer wherever possible, as mixing insurers can complicate cashless claims at the hospital.

Why is buying health insurance for parents early so important?

Buying health insurance for parents early gives them access to better plans while they are still relatively healthy. Pre-existing disease waiting periods clock start from day 1 of the policy, so buying early means full coverage kicks in sooner. Many plans also cap entry age at 60 or 65, which means delaying can close the door on good options entirely. Premiums also rise steeply with age. A family floater for parents aged 65 to 67 can cost nearly ₹30,000 more per year than one for parents aged 60 to 62.

What is the restore or recharge benefit in health insurance, and why does it matter for parents?

The restoration or recharge benefit refills your sum insured if it gets exhausted during the policy year. For parents who may need multiple hospitalizations in a single year, this benefit is critical. Care Supreme, for instance, offers unlimited automatic recharge, which can be used unlimited times, even for the same illness. HDFC ERGO Optima Secure's one time Restore Benefit can also be upgraded to unlimited refills via an add-on. Always check whether the restoration applies to the same illness or only to unrelated conditions, as this affects its usefulness in practice.

What is copayment in health insurance, and should parents avoid it?

Copayment means you pay a fixed percentage of the hospital bill yourself, while the insurer covers the rest. For example, a 20% copay on a ₹5 lakh bill means you pay ₹1 lakh out of pocket. For parents, this can add up significantly since hospital bills tend to be higher at older ages. At Ditto, we strongly recommend choosing a plan with no copay for parents. Many senior citizen-specific plans have mandatory copay clauses, which is one reason comprehensive plans without this restriction are preferred when available.

Is corporate health insurance enough for parents, or do they need a separate policy?

Corporate health insurance can cover parents from day 1, with no waiting periods and no questions about pre-existing conditions, making it a useful bonus layer. However, at Ditto, we advise against treating it as the only cover. Corporate plans disappear when you change jobs, retire, or when your employer revises the policy. They are also not portable in most cases. Use corporate cover as a supplementary layer and invest in a personal health insurance plan for your parents as the primary, long-term protection.

What is the best health insurance plan for parents above 60, specifically?

At Ditto, we recommend HDFC ERGO Optima Secure as the strongest plan for parents aged 60 and above. It has a 96.71% claim settlement ratio (FY 2022-25), covers 13,000+ hospitals, and carries no copay, no room rent limits, and no sub-limits. For parents with pre-existing conditions like diabetes or high BP, the ABCD Chronic Care add-on cuts the waiting period from 3 years to just 30 days. If underwriting is a concern, Aditya Birla Activ One MAX is a strong alternative with smoother approvals and competitive premiums. Care Supreme stands for early PED coverage and no loading charges.

What is the difference between Optima Secure and Optima Secure Plus for parents?

Both plans are from HDFC ERGO and share a strong foundation, insurer, and claims experience. The key difference is that Optima Secure+ includes an in-built unlimited restoration benefit and a 100% sum insured bonus with no upper cap on accumulation, making it better suited for younger parents who want more room to grow coverage over time. Optima Secure, on the other hand, is also available to parents over 60. At Ditto, the recommendation is simple: parents over 60 should choose Optima Secure, and those under 60 can consider Optima Secure+ for the additional headroom.

What is a waiting period in health insurance, and how does it affect coverage for parents?

A waiting period is the time after buying a policy during which certain conditions are not covered. There is a 30-day waiting period for everything apart from accidents. A 2-year compulsory waiting period for slow-growing conditions like cataract. For pre-existing diseases like diabetes or hypertension, plans have a waiting period of 2 to 3 years. This means that if your parent is diagnosed with, or has a history of, a condition, claims related to it will be rejected during that window. For parents, this makes buying early crucial since the clock starts from day 1 of the policy.

How does medical inflation in India affect the health insurance cover I should buy for my parents?

Medical inflation in India is running at 13% annually, meaning hospital costs are rising significantly faster than overall inflation. A heart bypass surgery that costs ₹5 lakh today could cost over ₹9 lakh in 5 years at that rate. This is why, at Ditto, we recommend a minimum sum insured of ₹15 lakh to ₹25 lakh for parents today, rather than the ₹5 lakh covers considered adequate a decade ago. Plans with strong cumulative bonus features can help your parents' effective cover grow over time without a proportional rise in premium.

What are the common mistakes people make when buying health insurance for parents?

The most common mistake is going for the cheapest plan, which often comes with copay, room rent caps, and sub-limits that quietly reduce payouts at claim time. Another big one is waiting too long to buy. Every year you delay, premiums rise, and the risk of a health condition blocking eligibility increases. Not disclosing pre-existing conditions is also a serious error and can lead to outright claim rejection. At Ditto, we also see families relying entirely on corporate cover, which can vanish when you switch jobs.

What is the difference between individual and floater health insurance for parents?

In an individual plan, each parent gets their own dedicated sum insured. In a floater plan for two parents, both share a single sum insured. A floater is generally more affordable and works well when both parents are healthy, have less of an age gap, and are unlikely to be hospitalized simultaneously. However, if one parent has a serious illness requiring extended treatment, they can exhaust the shared cover, leaving the other parent without adequate protection. At Ditto, we suggest a floater for most parents as a starting point, and individual plans when their health profiles differ significantly.

What is premium loading in health insurance, and how does it affect parents' policies?

Premium loading means an insurer charges you more than the standard premium because of a specific health condition disclosed during the application process. For example, if your parent has a history of hypertension, the insurer may load the premium by 10% to 50% on top of the base rate. This range can vary from insurer to insurer. In some cases, instead of loading, the insurer may permanently exclude that specific condition from coverage. For parents above 60 with multiple conditions, loading is common. At Ditto, we recommend always evaluating the final premium offered after underwriting, not just the advertised base price.

What is cashless hospitalization, and how do I check if my parents' hospital is covered?

Cashless hospitalization means the insurer settles the hospital bill directly with the hospital, so you do not need to pay upfront and claim reimbursement later. This requires the hospital to be in the insurer's network. To check coverage, visit the insurer's official website and search their hospital network by city and pincode. A wide national network means little if the quality hospitals near your parents are not empaneled. At Ditto, we recommend verifying which hospitals your parents use regularly before finalizing a plan, rather than just checking the total network size.

Can NRI or overseas indians buy health insurance for parents living in India?

Yes, Non-Resident Indians (NRIs) can buy health insurance for parents living in India. Most Indian insurers allow the policyholder to be an NRI as long as the insured parents reside in India. The policy covers hospitalizations within India, and premiums can typically be paid through NRE or NRO accounts. Tax benefits under Section 80D (under the old regime) are available only if you file taxes in India. At Ditto, we recommend NRIs treat this as a priority since parents living alone in India without a health cover face the highest financial risk in a medical emergency.

What is the difference between reimbursement and cashless claims in health insurance for parents?

In a cashless claim, the insurer settles the bill directly with the hospital, so your parents do not need to arrange funds upfront during a medical emergency. In a reimbursement claim, you pay the full hospital bill first and then submit documents to the insurer for reimbursement, a process that can take weeks. For parents, especially those who may be hospitalized without family present, cashless claims are far more practical. At Ditto, we recommend always confirming that your parents' preferred hospitals are in the insurer's cashless network before buying a plan, not after.

What happens to my parents' health insurance if the insurer withdraws the plan?

If an insurer decides to withdraw a health insurance plan, IRDAI guidelines require them to offer existing policyholders a migration option to a comparable plan without losing their waiting-period and moratorium-period credits and no-claim benefits. Since January 2025, insurers also needed IRDAI's prior approval before withdrawing any plan specifically designed for senior citizens, adding an extra layer of protection. At Ditto, we recommend choosing plans from insurers with a strong, stable product history and low complaint volumes. A plan that has been running for several years with consistent terms is generally a safer long-term bet for your parents.

What are the IRDAI timelines for health insurance claim settlement in India?

IRDAI mandates specific timelines that insurers must follow when settling health insurance claims. For cashless claims, the insurer must respond to the initial authorization request within 1 hour and communicate the final discharge authorization within 3 hours of receiving the request. For reimbursement claims, the insurer must settle the claim within 15 days of receiving all required documents. At Ditto, we factor in real-world cashless approval speed when recommending plans for parents, since a policy that delays authorization during a medical emergency is a serious problem regardless of what the policy terms say.

Customer Reviews

4.9

20915 reviews

Ditto is doing really great. Absolutely spam free- that's the best part. They don't talk to you like they are forced to sell the product. It's more like, helping us buy better. Advisor Nuha was very patient and answered all my questions with clarity. Thanks for the service

I

INDHUMATHI M

Loved the service! Maheta Nidhi Hitesh was incredibly helpful and knowledgeable. She guided me through the whole process and made everything super easy to understand. I really appreciated how patient she was with all my questions—there was no pressure at all, just clear and honest advice. Honestly, I'm very happy with my experience at Ditto so far. Highly recommend!

RK

Ragul Kumar

I had a great experience with Ditto while exploring health insurance options. The process was smooth and everything was explained clearly.

A special thanks to Swaroop SK for patiently answering all my questions and guiding me through the policy details without any pressure. The transparency and support made it much easier to understand and choose the right plan.

Really appreciate the assistance!

PS

Pulkit Singh

Had a great experience with Ditto Insurance. Ishita Sudrania was extremely helpful in guiding me through choosing the right term plan. There was no spamming or sales pressure, and all my questions were patiently answered. She also assisted me thoroughly with the entire application process. Highly recommend!

SS

Samil Shah

I had a great experience with Ditto while filing my health insurance claim. Their team guided me clearly through the entire process, helped with the required documents, and promptly answered all my queries. Their support made the claim process much smoother and less stressful. Highly appreciate their assistance.