Quick Overview

Considering the ongoing geopolitical instability, medical costs in India are expected to increase by 10% to 50%. This sharp increase means that coverage amounts, which once seemed adequate, may no longer offer sufficient financial protection. Hence, a ₹50 lakh health insurance policy offers a stronger cushion against large hospitalization bills.

This guide explains ₹50 lakh health insurance, including plan options, premiums, and the mistakes that can impact your coverage.

Is a ₹50 Lakh Health Insurance Cover Enough for You in 2026?

A ₹50 lakh sum insured offers comprehensive coverage against long-term illnesses, sudden emergencies, or black swan events like COVID-19 (an extremely unpredictable occurrence that has a massive impact) without creating a significant financial burden.

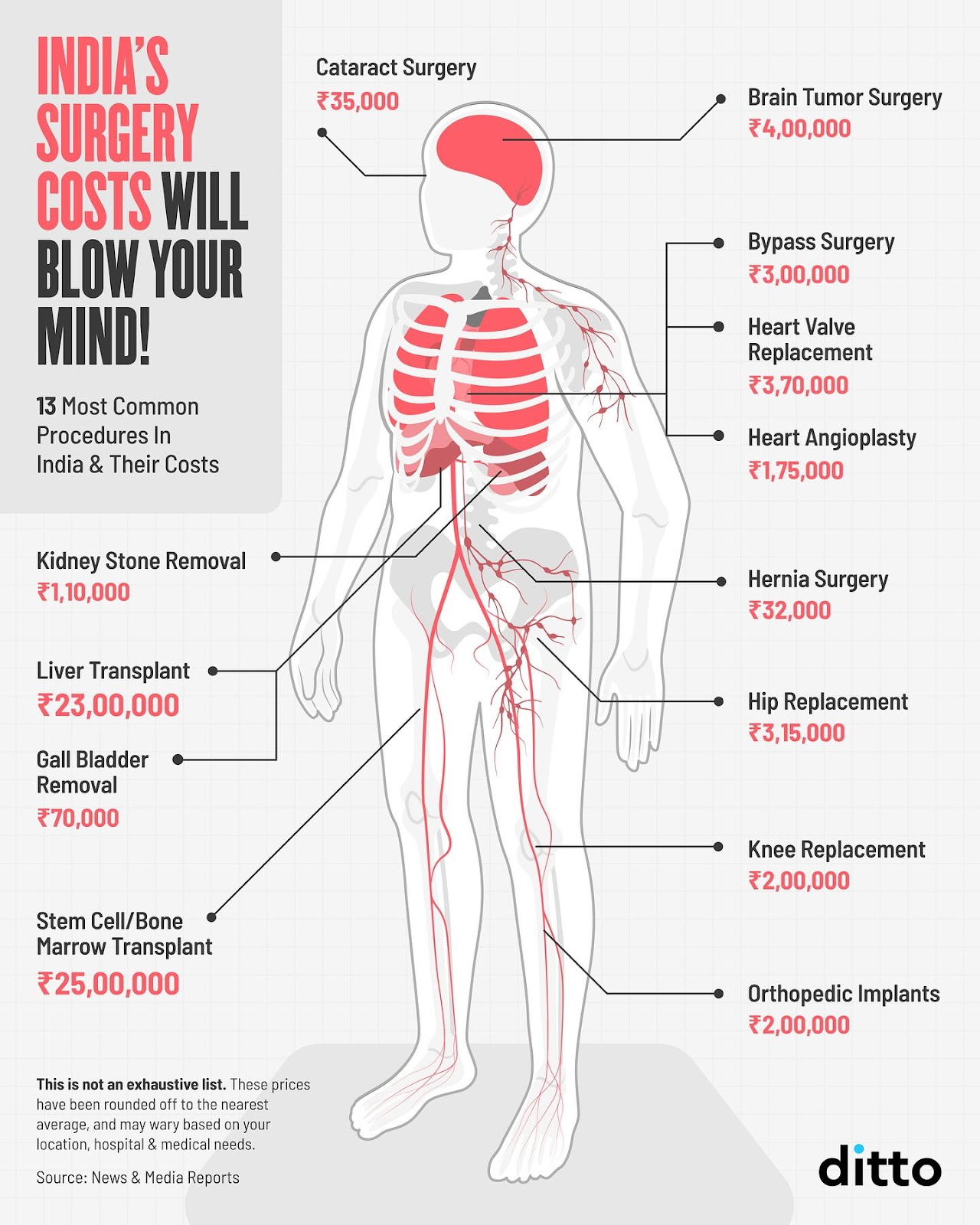

The infographic below shows treatment costs to help you judge whether a ₹50 lakh cover makes sense.

What is Included in a ₹50 Lakh Health Insurance Policy?

- Medically necessary hospitalization for conditions, including critical illnesses like cancer, heart disease, and diabetes.

- Extra coverage in the form of a bonus on top of the ₹50 lakh base sum insured.

- Restoration benefits that recharge your sum insured if it gets exhausted during multiple hospitalizations in the same year.

- Daycare procedures like cataract surgery, hernia repair, and knee replacement surgeries.

- Domiciliary (at-home treatment) and AYUSH treatments.

- Non-medical expenses like gloves, syringes, and PPE kits.

- Pre- and post-hospitalization expenses, typically 60 days before admission and 90 to 180 days after discharge.

Note: The exact benefits depend on the insurer and the selected plan.

Best Health Insurance Plans With ₹50 Lakh Sum Insured

Note: CSR stands for claim settlement ratio, and ICR denotes incurred claims ratio. For more details, refer to our guide on the best health insurance plans in India 2026.

Premiums for ₹50 Lakh Sum Insured

Here’s a comparison of sample premiums for a tier-1 city (New Delhi, 110001). The profiles considered here are healthy and have no pre-existing diseases.

Note: A stands for adult and C denotes child. These are indicative figures.

Factors that may affect your ₹50 lakh health insurance premium are age, existing health conditions, and location.

Key Insight

Common Mistakes to Avoid While Choosing a ₹50 Lakh Sum Insured

- Ignoring the Claim Settlement Ratio: A high sum insured is not helpful if the insurer rejects your claims. Having a higher CSR is a useful indicator, although it should not be the only thing you base your decision on. We recommend a CSR of over 90%.

- Not Reviewing Your Cover Periodically: A ₹50 lakh cover is sufficient. However, it is not safe from inflation, so it's worth reviewing your policy every 3 to 5 years. Not to replace it, but to make sure it still fits your life stage, family size, and is enough for your preferred hospitals.

- Choosing a plan with limits: To reduce premiums, you might choose a high sum insured plan with sub-limits. For example, if your plan caps room rent at ₹5,000 per day, and you opt for a ₹10,000 room, the insurer will proportionately reduce your entire bill, not just the room cost.

- Misunderstanding Restoration: Most people assume that restoration applies to the total coverage. This is not true for most plans. Your restoration applies only to the base policy, not to accumulated bonuses. Restoration kicks in only after the base sum insured is partially or fully used.

- Assuming a Family Floater is Always Better: In a family floater policy, the sum insured is shared among all members. For families with older members or complex PEDs, separate individual policies often make more sense, even if the upfront cost is higher.

Why Choose Ditto for Health Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or chat on WhatsApp with us now!

Conclusion

A ₹50 lakh health insurance policy is ideal if you:

- Live in a metro city like Delhi, Mumbai, or Bengaluru, where hospital costs are significantly higher.

- Are looking to cover your family, especially with elderly parents.

- Have a pre-existing disease like diabetes, hypertension, or heart disease.

- Want long-term peace of mind and stable protection.

If budget is a concern, we recommend starting with a ₹15 to ₹25 lakh cover. With bonuses, restoration benefits, and the right plan, your effective coverage grows over time and keeps pace with inflation. Just remember that increasing your base cover later can get harder if any health conditions develop in the meantime.

If you’re starting your health insurance search, you can check our guide on how to choose health insurance to learn about other factors beyond the sum insured.

Frequently Asked Questions

Last updated on: