Quick Overview

Founded in 2001, Kotak Mahindra Life Insurance (commonly known as Kotak Life) is part of the Kotak Mahindra Group. Over two decades, it has built a sizable presence across India with a diversified product mix spanning protection, savings, ULIPs, retirement, and child-focused plans.

Kotak Life’s term product range includes pure term insurance like Kotak E-Term and Signature plan, return of premium variants, and IRDAI-mandated products such as Saral Jeevan Bima.

If you’re evaluating Kotak Life Insurance policy details, it’s important to compare plan features carefully rather than relying only on premiums.

Kotak Life Insurance Performance Metrics

As of FY 2024–25, Kotak Life Insurance manages Assets Under Management of ₹91,807 crore, placing it among the leading private life insurers in India by AUM. The insurer has consistently maintained a claim settlement ratio above 98% and a solvency ratio well above the regulatory requirement, indicating stable financial strength and operational reliability.

Note: Kotak Life Insurance has a strong scale, stable claim performance, low complaint levels, and solid financial strength. However, its claim settlement ratio is slightly below the industry average and trails leading players such as HDFC Life, Axis Max Life, and Bajaj Life.

For a closer look at insurer metrics, explore Ditto Data Lab. It includes term insurance data from public disclosures that have been carefully curated by our team over the years.

Take Note: If you’re buying life cover for the first time, having a simple term insurance checklist can make things much easier. It helps you figure out how much coverage you actually need, how long the policy should last, and which riders are worth adding.

Top Plans Offered by Kotak Life Insurance

Types of Plans Offered by Kotak Life Insurance

- Term Plans: Kotak E-Term Plan, Kotak Signature Term Plan, Kotak Term Plan, Kotak Saral Jeevan Bima.

- Return of Premium (ROP) Term Plans: Kotak Gen2Gen Protect (Life ROP & Legacy ROP options)

- ULIPs (Unit Linked Insurance Plans): Kotak e-Invest, Kotak Single Invest Plus, and Kotak Wealth Optima.

- Savings & Endowment Plans: Kotak Assured Savings Plan, Kotak Premier Life Plan, and Kotak Sampoorn Bima Micro-Insurance Plan.

- Retirement & Pension Plans: Kotak Lifetime Income Plan, Kotak Assured Pension.

Premium Comparison for Kotak Term Plan’s Flagship Term Plan

Note: Kotak e-Term is competitively priced for younger buyers, particularly at age 25, where second-year premiums remain under ₹8,500. The premiums shown reflect second-year onwards rates and exclude first-year discounts. For ₹2 crore coverage till 65, the Kotak Signature Term Plan offers strong pricing, especially for female policyholders, who receive a 16% premium discount across policy years.

Riders Available in Kotak Term Plans

1) Accidental Death Benefit Rider: This rider pays an additional lump sum amount (over and above the base sum assured) if death occurs due to an accident. It is useful for individuals in high-travel or higher-risk professions who want extra financial protection against accidental fatalities.

2) Critical Illness Plus Rider (37 Illnesses): This rider pays a lump sum if the policyholder is diagnosed with any of the listed 37 critical illnesses, subject to a 90-day waiting period and 30-day survival period.

The payout can be used for treatment costs, income replacement, or lifestyle adjustments. However, coverage is limited strictly to the predefined illness list; it does not function like a comprehensive health insurance policy.

This rider is not automatically available with every Kotak Life Insurance plan by default. It is an optional add-on rider that can be attached only to select term plans like Kotak E-Term, Kotak Signature Term Plan, and Kotak Gen2Gen Protect, wherever Kotak specifically lists it as a rider option. So, it is available only if the chosen plan explicitly offers it and you select it at the time of purchase.

3) Permanent Disability Benefit Rider: If the policyholder suffers total and permanent disability due to an accident, this rider pays 120% of the rider sum assured in installments over five years. This helps replace income in case the individual is unable to work.

Unlike some insurers like Bajaj Life that automatically include a waiver-of-premium benefit on disability across most term plans, Kotak does not consistently bundle this feature as a standard in-built benefit. In many cases, waiver functionality is available only under specific plan options (like Life Secure variants) or through separate rider structures.

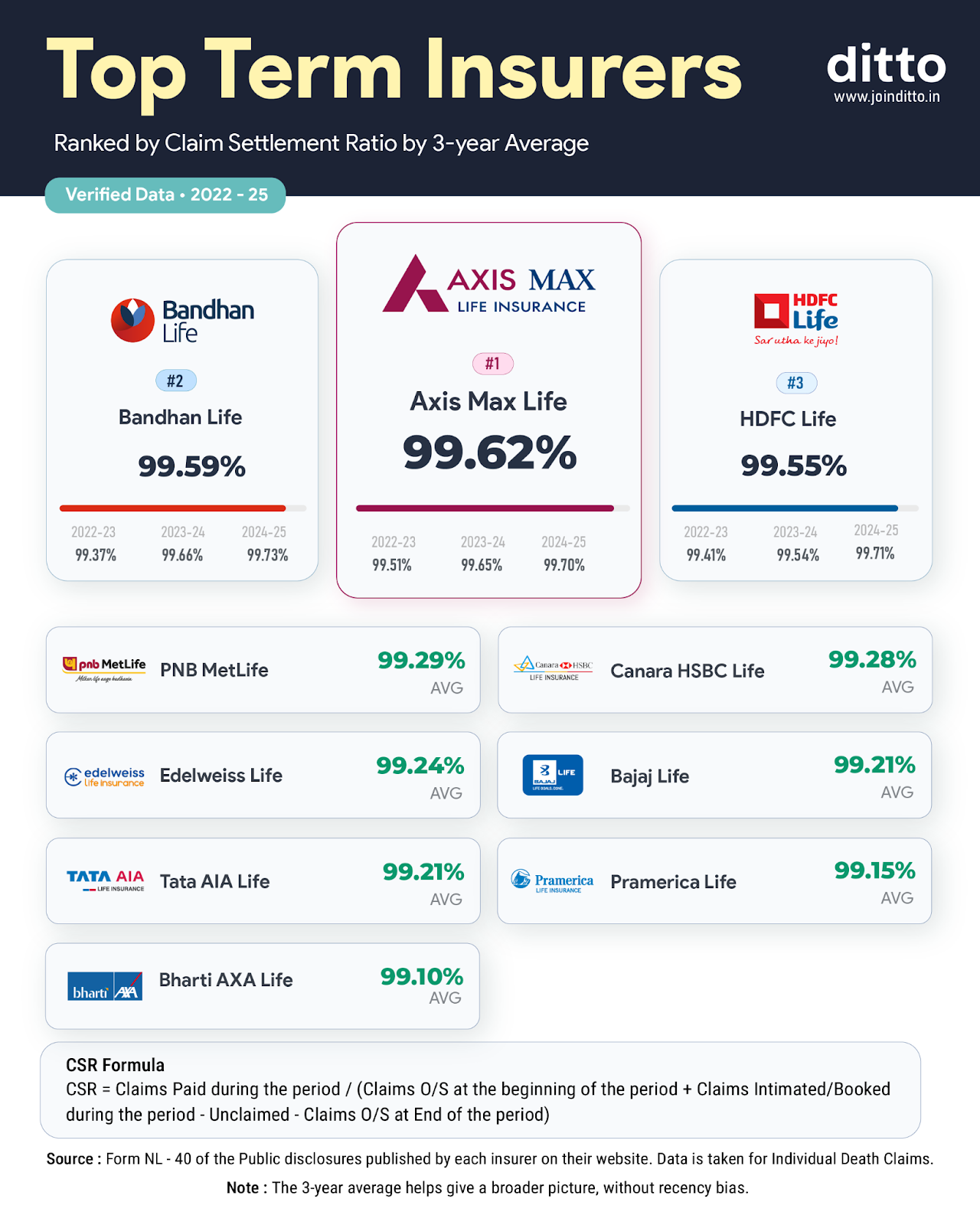

Top 10 Life Insurance Companies in India by Claim Settlement Ratio

Note: The CSR shown here represents the insurer’s overall performance and is not specific to the term insurance segment alone.

Kotak Life Insurance consistently ranks among the top private life insurers in India by assets under management and new business premium. While its CSR is broadly in line with industry leaders rather than significantly ahead, the company stands out for its strong solvency position, relatively low complaint ratio, and competitive pricing in the term segment, especially for female policyholders.

Its financial scale and stable operational metrics make it a credible and dependable player within the top tier of private life insurers.

Why Choose Ditto for Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp with our expert IRDAI-certified advisors.

Ditto’s Take

Kotak Life Insurance offers reliable protection products backed by strong claim metrics and solid solvency levels. Its premium pricing is competitive, especially for women policyholders, and complaint ratios are better than the industry median.

However, many of its plans lack modern in-built features such as instant claim intimation payouts or automatic cover continuance in case of premium break, which several newer insurers now offer. Additionally, commonly sought riders like waiver of premium are not consistently available across its portfolio.

If you prioritize stability and brand strength, Kotak Life Insurance is a dependable choice. If you want feature-rich modern protection designs, you may want to compare alternatives.

If you are looking for comprehensive term coverage that align your medical needs, we recommend the best term insurance companies for 2026.

Disclaimer: Kotak Life Insurance is not a partner insurer of Ditto. Our assessment here is completely independent and based solely on publicly available data and the evaluation framework we use for all insurers.

If you want to understand how Ditto reviews insurers across claims, complaints, business strength, and product suitability, read our methodology here. Please check the insurer’s official website for the latest available information.

Frequently Asked Questions

Last updated on: