Overview

It’s true that an insurance purchase is not an investment. However, health insurance policies are essential financial protection tools. Such plans are meant to safeguard your savings in case you ever need to be hospitalised, are diagnosed with an ailment that needs prolonged treatment, or meet with an accident. Considering such circumstances (and the rising cost of healthcare services), you must avail of a health insurance policy.

Now, the question is, how do you choose a health insurance plan? We say, don’t!

We have picked up two of the country's most “well-heard of” health insurance providers: HDFC Ergo and TATA AIG health insurance. Who do you think will win this? Let’s find out!

Tata AIG Health Insurance vs HDFC Ergo: Peformance Metrics

HDFC Ergo Health Insurance or TATA AIG Health Insurance: Which is Better?

Founded in 2002 as a joint venture between HDFC and ERGO International AG, HDFC Ergo has become one of India's largest health insurers. Despite slightly higher costs, its comprehensive policies and extensive network of cashless hospitals contribute to its reputation as one of the country's most credible health insurance providers.

Established in 2001 through a partnership between Tata Group and American International Group, TATA AIG has rapidly grown in the industry, garnering substantial praise. While its health insurance plans may be relatively expensive with no distinctive features, some policies provide coverage for international treatments and maternity-related expenses.

Since both insurers have a couple of drawbacks that you need to consider, this will be an interesting comparison. While we have summarised the standpoint of these two general insurance providers as health insurers, a data-based comparison will be a better way to go. As far as data are concerned, we have gathered 3 years' worth of information (2020 to 2023) to get a consistent insight into the overall performance of the insurers.

Claim Settlement Ratio (CSR)

Claim Settlement Ratio is one of the most well-known metrics when determining the credibility of a health insurance provider. It is computed by finding the % between the total number of claims settled by an insurer over a year and the total number of claims filed to the insurer over the same year.

While this gives you a partial idea about the claim settlement efficiency of the insurer, what CSR fails to reflect is how fast the claims are settled and to what extent. However, it’s still a start.

So, here is an insight into the CSR of HDFC Ergo health insurance vs TATA AIG health insurance for 2022 to 2025.

CONCLUSION: HDFC Ergo takes the win here with a close-to-perfect CSR. On the other hand, since we recommend that you follow through with insurers with a 90+ score in CSR, we can safely say that TATA AIG is just a little behind!

Incurred Claim Ratio (ICR)

Where CSR falls short of reflecting how well the claims have been settled, Incurred Claim Ratio fills in the gap. ICR is calculated by drawing a % between the total amount involved in claim settlement for an insurer across a year and the total premium collected by the insurer in the same year.

The ICR of an insurer is particularly effective if you want to draw insight into the financial stability and long-term financial potential of the insurer to settle claims. The extremes of ICR reflect either

- the insurer is too focused on making profits and thus neglecting valid claims raised by the clients or

- if the provider is settling too much in claims and steadily losing their financial foothold, therefore heading towards an unstable business situation.

The ideal range of ICRs for health insurance providers would be between 50 to 70 or slightly higher.

Here’s how the ICRs are for HDFC Ergo and TATA AIG health insurance from 2022 to 2025:

CONCLUSION: TATA AIG is the closest to the ideal range of ICRs and, hence, takes the win. However, even though HDFC Ergo has a slightly higher ICR, it indicates that the insurer prioritises meeting its client requirements, which is good news for policyholders.

Volume of Complaints

TATA AIG and HDFC Ergo both have excellent reputations as health insurance providers. Their plans are generally comprehensive and cater to a vast pool of policyholders. However, as potential policyholders, you need to prioritise knowing whether such reputations are well-founded or not, that is, what kind of complaint records these insurers are looking at.

This will help you understand the overall operational efficiency of the insurer, its issues with overall claim settlement (since that is one of the most common reasons for complaints), etc.

Here is a look at the complaint volume for HDFC Ergo and TATA AIG for 2022 to 2025:

CONCLUSION: With one of the lowest complaint volume numbers in the industry, HDFC Ergo steals the win from TATA AIG. However, the complaint volume for TATA AIG is appreciable, too. Such low numbers are good indicators for both the providers showcasing their efficiency in meeting client requirements.

Network Hospitals

The number of network hospitals for health insurance providers reflects their established reputation with medical facilities and ensures that you have convenient access to cashless treatment perks. This makes it a determining factor when choosing a health insurance provider. The more the number of partner hospitals, the higher your chances of having access to cashless treatments for scheduled and emergency medical attention.

Here is a look at the network of partner hospitals for both TATA AIG and HDFC Ergo health insurance providers -

CONCLUSION: TATA AIG health insurance wins with a close to 700 margin on HDFC Ergo. This score is impressive considering that TATA AIG has only a 1-year advantage over HDFC.

5. Major Plans From Tata AIG and HDFC Ergo

Why Choose Ditto for Health Insurance?

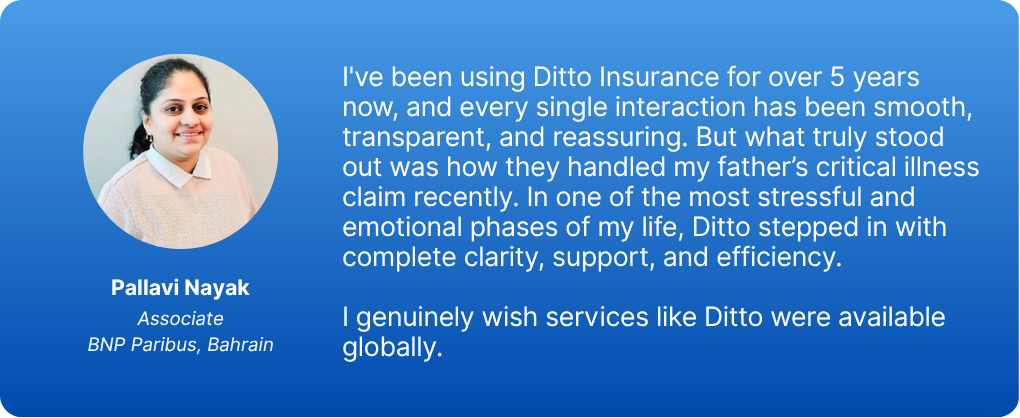

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Pallavi below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call now or chat over WhatsApp, slots fill up fast!

Conclusion

HDFC Ergo and TATA AIG offer almost identical (or close to) metrics that make this decision difficult. We would say that the decision would vary based on your health insurance policy. While some plans from TATA AIG are expensive, policies from HDFC Ergo, in general, tend to be more costly than the rest in its class. So,

- Factor in your pre-existing medical conditions,

- Take a look at suitable policies from both the insurers,

- Compare the add-ons available

- Compare the respective premiums.

Frequently Asked Questions

Customer Reviews

Last updated on: