Term insurance for the self employed becomes essential as there are no employer-backed benefits. A term plan for a self employed provides a safety net, ensuring the family can maintain their lifestyle, clear debts, and run the business if they pass away. Eligibility depends on Income Tax Returns (ITRs) and the computation of income, since insurers usually offer coverage ranging from 20 to 30 times the annual income.

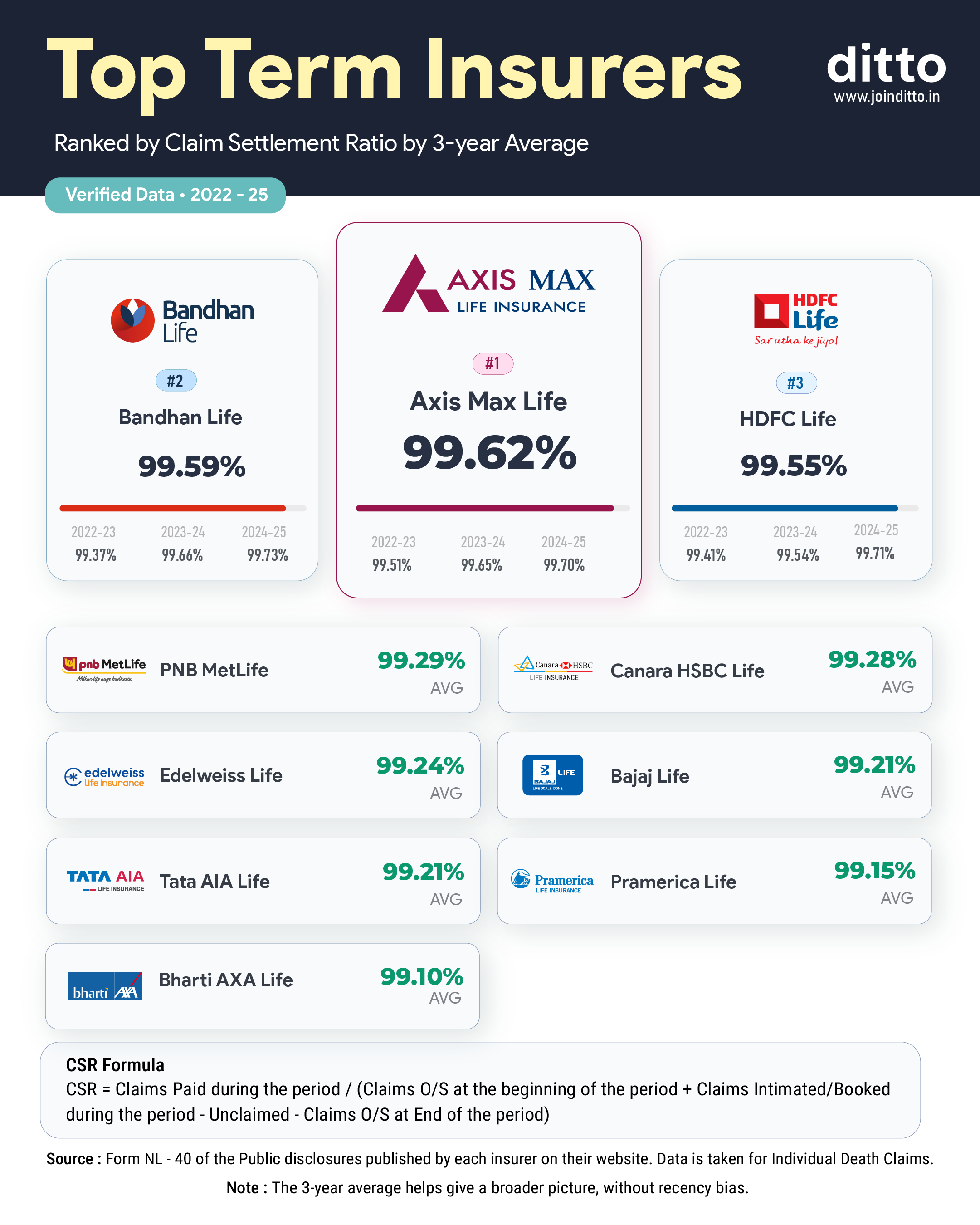

A 25-year-old self employed man can get a ₹2 crore term cover until age 70 for an annual premium of ₹17,000 to ₹22,000. Ditto’s top pick is Smart Term Plan Plus, backed by Axis Max Life, with a claim settlement ratio of 99.62% (average FY 2022-25).

This guide is ideal for self-employed professionals looking for the right term plan.

More than half of India’s workforce is self employed, with 56.2% in 2025 as per the PLFS annual report 2025. For this group, income security depends on personal effort, not an employer. That is why term insurance becomes essential, as it protects both your family and your business if your income stops suddenly.

This guide breaks down how term insurance works for self employed individuals, which plans stand out in 2026, and how to choose the right cover without making costly mistakes.

ICICI Prudential iProtect Smart Plus is a practical option for buyers seeking competitive pricing and useful features without added complexity.

ICICI Prudential

iProtect Smart Plus

4.3

Overall Rating

Insurer Rating

4.4/5

Customer Service

5.0/5

Feature Rating

3.8/5

Premium Rating

5.0/5

Key Features:

Life Stage Protection: Option to increase cover after marriage, childbirth, or home loan in eligible cases.

Instant Partial Payout: Early claim support with accelerated payout for eligible higher covers.

Smart Exit Benefit: Choice to exit after a defined period and receive eligible premiums back under selected variants.

Premium Break Option: Temporary pause on premiums for up to one year after regular payments, subject to terms.

Bottom Line:ICICI Prudential iProtect Smart Plus is a clean and well-balanced plan. It suits buyers who want essential features and strong brand confidence.

04

Bajaj Life

eTouch II

Bajaj Life eTouch II is a solid option for buyers who want affordable premiums and dependable core benefits.

Bajaj Life

eTouch II

4.2

Overall Rating

Insurer Rating

4.4/5

Customer Service

5.0/5

Feature Rating

3.4/5

Premium Rating

5.0/5

Key Features:

Terminal Illness Benefit: Early payout on diagnosis of terminal illness, up to ₹2 crore.

Premium Holiday Add-on: Option to temporarily skip premiums under eligible conditions while keeping cover active.

Early Exit Value: Available at older ages under selected terms and policy conditions.

Waiver of Premium: Future premiums will be waived on specified accidental disability or terminal illness events.

Bottom Line:Bajaj Life eTouch II is a value-focused plan that works well for cost-conscious buyers.

05

Aditya Birla Sun Life Insurance

Super Term Plan

Aditya Birla Sun Life Super Term Plan is a well-rounded option for those who prefer broader protection in a single policy.

Aditya Birla Sun Life Insurance

Super Term Plan

4.0

Overall Rating

Insurer Rating

3.7/5

Customer Service

5.0/5

Feature Rating

4.3/5

Premium Rating

5.0/5

Key Features:

Optional Critical Illness Cover: Lump sum payout for 42 listed illnesses with an accelerated payout of up to 50% of sum assured, capped at ₹50 lakh.

Terminal Illness Benefit: Early payout support on diagnosis of terminal illness. This ensures financial support during serious conditions.

Cover Continuance Benefit: Premium deferment option under specific conditions. This helps during temporary income challenges.

Early Claim Support: Includes partial payout on claim intimation and exit value under selected terms.

Bottom Line:Aditya Birla Sun Life Super Term Plan is suitable for buyers seeking both life cover and illness-related financial support in a single plan.

Talk to an expert today and find the right insurance for you.

When purchasing a term plan, it’s important to look at insurer metrics such as the Claim Settlement Ratio (CSR). Check the infographic to learn which term insurers rank among the top 10 for CSR.

Eligibility Criteria for Term Insurance for Non Salaried Person

Criteria

What Insurers Usually Check

Insight

Age

Entry starts from 18. Maximum entry age depends on the plan, usually between 60 and 65 years.

Buying early works in your favor, as premiums are locked in for the entire policy tenure. Younger applicants get smoother approvals and much lower premiums.

Income Proof

ITRs, income computation, balance sheet, Profit and Loss (P&L), bank statements, Form 26AS, Goods and Services Tax (GST) returns, or Chartered Accountant (CA) certified financials.

This is the biggest filter. Insurers want to see whether your income supports the cover you are requesting.

Sum Assured Eligibility

Based on income, age, existing cover, and internal underwriting rules. It is usually 20-30x annual income.

Your cover must match your income. A low declared income will not support a very high sum assured.

Existing Life Cover

Details of all personal active life insurance policies across insurers must be shared.

Insurers check your total cover across companies. Hiding policies can create problems at the claim stage.

Medical History

Health conditions, smoking, alcohol use, family history, and test results.

Be fully honest. Health details matter more than income. Non-disclosure can lead to claim rejection.

Occupation Risk

Nature of work, travel, manual exposure, and involvement in high-risk industries.

Riskier jobs can mean higher premiums or stricter checks compared to low-risk roles.

Education / Financial Profile

Education level, city category, credit behavior, banking activity, and digital income trail.

This works in the background. It can influence decisions, especially when income documents are limited.

Key Insights:

For self-employed applicants, commission-based earnings do not qualify as reliable income, nor do trading income. Insurers generally focus on consistent, verifiable income as shown through ITRs (filed in the applicant's name) and financial records, rather than on the profession itself.

There is no fixed income rule for term insurance. For ₹1 crore or higher coverage, insurers usually prefer declared annual income of ₹5 lakh or more.

Features of Term Insurance for Business Owners

Higher Sum Assured Flexibility: Entrepreneurs face greater financial exposure due to loans and family responsibilities. Higher sum assured options ensure that protection matches real-life liabilities.

Premium Break Options: This feature allows a temporary pause in payments without losing coverage, which helps during periods of low cash flow.

Flexible Payout Structures: Nominees can choose between a lump sum and a monthly income.

Exit Options: Some plans offer premium refund or early exit features. While not essential, they appeal to buyers who prefer some value back at the end of the term.

Limited Pay Options: Many business owners prefer to make payments during strong earningsyears. At Ditto, we recommend limited pay for self employed individuals as it allows premiums to be paid during peak earning years and removes the risk of policy lapse during periods of lower or unstable income later in life.

Note: Insurers consider net profit when assessing term insurance for business owners, but it is evaluated alongside other factors, including ITR, income computation, business stability, and more. The core principle is that insurers do not insure turnover, but they assess documented earning capacity.

Sample Premiums Across Ages

Age

Axis Max Life Smart Term Plan Plus

HDFC Life Click 2 Protect Supreme Plus

ICICI iProtect Smart Plus

25 (Male)

₹18,952

₹21,424

₹17,184

25 (Female)

₹16,110

₹18,209

₹14,606

30 (Male)

₹23,234

₹27,000

₹21,449

30 (Female)

₹19,750

₹22,951

₹18,232

35 (Male)

₹29,362

₹35,945

₹28,520

35 (Female)

₹24,958

₹30,553

₹24,242

Note: The premiums shown are indicative and based on non-smoker self employed profiles earning ₹10 lakh annually in Delhi (110010) for a ₹2 crore cover up to age 70 without first-year discounts.

Importance of Term Insurance for Self Employed/Business Owners

01

Stability Despite Business Ups and Downs

Incomes can fluctuate with market cycles or seasonal demand. A term plan ensures your family stays financially secure even if your business income becomes unpredictable.

02

High Cover at a Low Cost

Term insurance offers extensive coverage at an affordable premium. It remains a practical option even during periods of lower income.

03

Protects Personal Assets

Without adequate cover, families may need to sell savings, property, or investments. Term insurance helps avoid such forced decisions.

04

Covers Outstanding Debts

Business loans with personal guarantees can burden the family. A term plan ensures these liabilities are cleared without affecting personal wealth.

05

Protects Personal Wealth and Assets

Without adequate life cover, families may have to dip into savings, sell investments, or liquidate property to cover loans and daily expenses. Term insurance helps preserve long-term personal wealth.

Ditto’s Expert Insights on Term Insurance for the Self Employed

Clear Income Proof Builds Trust: Keep at least 2 to 3 years of ITRs, Form 26AS, and CA-certified income statements ready. These documents help insurers assess income consistency and build confidence in your financial profile during insurer underwriting.

Accurate Reporting Improves Eligibility: Always report income honestly and consistently. Declaring very low profits can limit your eligible cover, while accurate reporting improves your chances of securing a higher sum assured.

Keep Premium Payments Foolproof: Choose annual or half-yearly premium payments to reduce the risk of missed installments. You can maintain a separate bank account with 1 to 2 years of premiums and enable auto-debit.

Expert Guidance Makes a Difference: An experienced advisor like Ditto can structure your application better, explain income fluctuations clearly, and coordinate with underwriters. This improves your chances of approval and helps you secure suitable coverage faster.

How to Choose the Right Cover Amount for a Self Employed Person?

For self employed individuals, the ideal term insurance cover should protect your family’s lifestyle, replace your income, and account for business loans or financial responsibilities. Since self employed income can fluctuate, it is important to choose a realistic cover amount based on long-term earning stability rather than short-term spikes. For a more accurate estimate, use our online term insurance calculator to understand how much coverage may truly suit your financial situation.

Income Proofs & Documents Required

Identity Proof, like a PAN card or a passport, for basic identity verification.

A recent passport-size photograph is needed for insurer records.

Address proof like an Aadhaar card, passport, or driving license.

Income proof, such as ITR and CA-certified income computation for the last 2 to 3 years.

Details of any current life insurance policies must be disclosed to ensure an accurate assessment of total coverage across insurers.

A canceled cheque or bank statement showing the account holder's name, account number, Indian Financial System Code (IFSC), and Magnetic Ink Character Recognition (MICR).

Medical records (if applicable) as per the underwriting requirements set by the insurer.

Take Note: Some newer term insurance plans for self employed individuals, such as Bajaj iSecure II and ICICI iProtect Super, allow coverage even without standard income proofs like ITRs or CA certificates. Instead, insurers assess financial strength through surrogates such as credit scores, bank balances, spending patterns, or even the vehicle's Insured Declared Value (IDV).

How to Pick the Right Term Insurance for a Non Salaried Person?

01

Choose the Right Cover Amount

Consider all key factors, including existing loans, monthly household expenses, future goals, and inflation. This ensures your family can continue with their lives without financial pressure if income stops.

02

Select the Right Policy Term

Pick coverage that ideally lasts till age 60 to 70. Most liabilities are reduced by then, and dependents often become financially independent.

03

Protects Personal Assets

Without adequate cover, families may need to sell savings, property, or investments. Term insurance helps avoid such forced decisions.

04

Use Limited Pay Smartly

Pay premiums during strong earning years so your cover stays active even if income becomes unstable later.

05

Check Insurer Reliability

Review insurer metrics like CSR, complaint levels, and business size.

06

Add Useful Riders

Include riders such as critical illness cover or a waiver of premium. These help protect you during illness or disability when income may stop.

See the infographic below to understand which riders to consider and which ones to avoid.

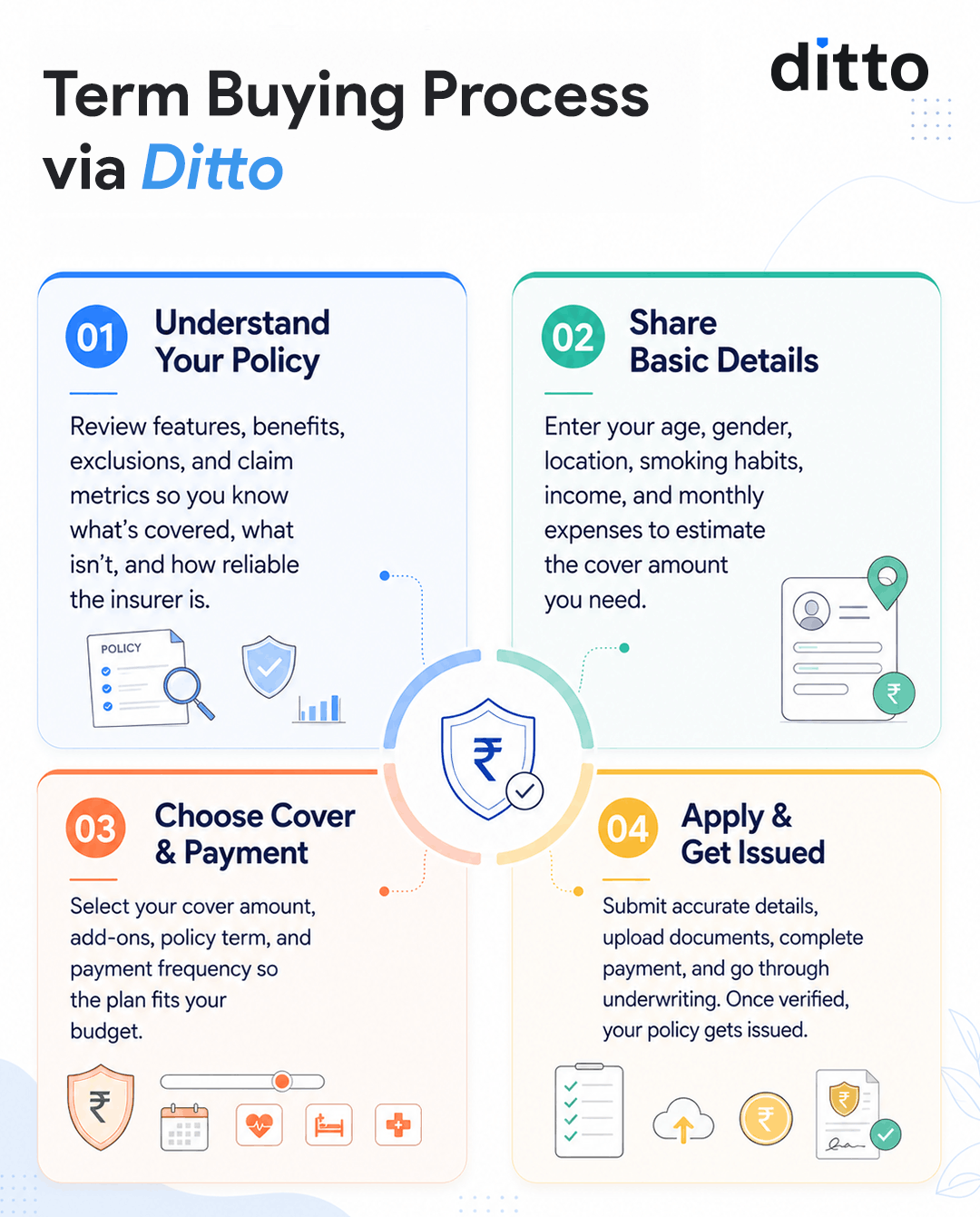

How to Buy Term Insurance for Self Employed/Business Owners From Ditto?

Buying term insurance online through Ditto is simple and convenient. At Ditto, we help you navigate underwriting, coordinate with insurers, and reduce delays caused by document checks for self employed profiles. We also guide policy selection and ensure smoother approvals.

Take a look at the infographic to understand how the process works.

At Ditto, the premium remains the same as the insurer’s official online price, with all available discounts passed directly to you at no extra cost. We help throughout the entire journey, from plan comparison and proposal form filling to underwriting support and policy issuance. Most importantly, our support does not end after purchase. We also assist families during the claims process, helping with documentation, coordination, and insurer communication when it matters the most.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Aaron below love us:

No-Spam & No Salesmen

Rated 4.9/5 on Google Reviews by 15,000+ happy customers

Backed by Zerodha

Dedicated Claim Support Team

100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call or chat on WhatsApp now!

Ditto’s Verdict on Term Insurance for the Self Employed

Term insurance works best when it is simple, consistent, and structured around income stability. For self employed individuals, the real challenge is not just buying a policy, but ensuring it stays active through income ups and downs.

Additionally, for most self employed individuals and business owners, financial protection should begin with health insurance first, followed by term insurance and a strong emergency fund built alongside both. A medical emergency can disrupt income immediately, while term insurance protects your family and liabilities if something happens to you.

Full Disclosure

This article is purely for informational purposes and offers an unbiased review of plans from both our partner and non-partner insurers. The information has been sourced from IRDAI reports, insurer websites, and other publicly available data. Explore more about how our experts evaluate term plans through Ditto’s cut.

Frequently Asked Questions

Can self employed people get term insurance in India?

Yes, self employed individuals can easily get term insurance in India. The process is similar to that of salaried applicants, but documentation differs. Instead of salary slips or Form 16, insurers rely on ITRs, CA-certified income computation, and bank statements from the last 2 to 3 years. At Ditto, we regularly assist self employed applicants in aligning their income profile with suitable insurers and plans. Since over 56.2% of India’s workforce was self employed in 2025, most insurers have dedicated underwriting processes designed for this segment.

What documents do I need to buy term insurance if I am self employed?

The key documents include ITRs for the last 2 to 3 years, CA-certified income computation, Form 26AS, PAN card, Aadhaar or other address proof, bank statements, and a passport-size photograph. GST returns and business registration certificates can further strengthen your application. Only income from business or profession is considered for eligibility. Capital gains, F&O income, and interest income are excluded. At Ditto, we recommend preparing all documents in advance when applying for a term insurance, as missing paperwork is a common reason for delays in self employed underwriting.

Can I get term insurance without an ITR if I am self employed?

Yes, but coverage may be limited. Some newer term insurance plans like Bajaj iSecure II and ICICI iProtect Super allow alternative underwriting without standard income proof. They assess financial strength using credit score, bank balance, spending behavior, investments, or even vehicle IDV. Without ITRs, insurers usually cap coverage, often between ₹25 lakh and ₹2 crore, depending on financial signals. These options can be recommended for individuals with strong real earnings but limited documentation, as they improve access to fair coverage.

What is the best term insurance plan for the self employed in India in 2026?

At Ditto, our top recommendation is Axis Max Life Smart Term Plan Plus, with a 99.62% claim settlement ratio (FY 2022–25 average). It offers critical illness cover for up to 64 diseases, a premium waiver, premium break options, and an advance payout upon claim intimation. Other strong options include HDFC Life Click 2 Protect Supreme Plus and ICICI Prudential iProtect Smart Plus, both offering flexible payouts and life stage benefits. The right plan depends on income stability, documentation strength, and coverage needs.

Why is term insurance important for business owners or self employed individuals?

Self employed individuals and business owners do not have employer-provided life cover or retirement benefits. If income stops suddenly, families face immediate financial pressure. A term plan ensures continuity of daily expenses, loan repayments, and long-term goals such as education. It also protects personal assets from being sold to cover liabilities. Business loans with personal guarantees can pass financial risk to family members. At Ditto, we also highlight tax benefits under Section 80C of the old regime (now Section 123) and tax-free payouts under Section 10(10D), making it a highly efficient protection tool.

What is the limited pay option, and why is it useful for self employed buyers?

Limited pay allows you to complete premium payments within a fixed period, such as 10 or 15 years, while keeping coverage active for the full term. At Ditto, we recommend it strongly for self employed individuals because it ensures premiums are paid during high-income years. This reduces the risk of a policy lapse during later low- or unstable-income periods. It also removes long-term payment pressure and gives peace of mind that protection continues even if business income fluctuates or slows down in future years.

What is a premium break, and does it help self employed policyholders?

A premium break allows you to pause premium payments for a short period, usually up to one year, without losing your life cover. It is especially useful for self employed individuals whose income may fluctuate due to seasonal business cycles or market downturns. Plans like Axis Max Life Smart Term Plan Plus and HDFC Life Click 2 Protect Supreme Plus offer this feature. At Ditto, we consider it a practical safety net that helps maintain continuity during financial stress periods. However, the deferred premium must be repaid the next year, along with that year's premium.

What are income surrogates in term insurance for self employed individuals?

Income surrogates are alternative financial indicators that insurers use when standard income proof, like Income Tax Returns (ITRs) or salary slips, is unavailable or insufficient. For self employed applicants, insurers may check factors such as car IDV, home loans, Fixed Deposits (FDs), mutual funds, Systematic Investment Plans (SIPs), savings account balances, investments, or credit bureau records to assess financial stability. In some cases, these surrogates support eligibility even without proof of regular income. However, approval still depends on insurer underwriting rules, medical profile, business stability, and overall financial strength.

Should I buy term insurance before starting a business or after?

Buying term insurance before starting a business is usually better, especially if you are salaried. At that stage, income proof is stable, often backed by salary slips and Form 16, which makes underwriting easier and helps secure higher coverage at lower premiums. After becoming self employed, insurers may require 2 to 3 years of ITRs before offering high coverage. At Ditto, we recommend locking in a strong cover early, especially before taking out business loans or entering into financial commitments, since your approved cover remains fixed thereafter. Additionally, any change in occupation does not affect your term premiums once locked.

How does the MWP Act help self employed individuals with term insurance?

The Married Women’s Property Act (MWP Act) ensures that the term insurance payout goes only to your spouse and children, protecting it from business creditors. This is especially useful for self employed individuals with unsecured loans or personal guarantees, where liabilities may extend beyond the business. Without this structure, creditors could legally claim the payout in case of default. At Ditto, we recommend MWP Act policies for business owners to ensure the insurance benefit remains fully secured for the family, regardless of financial obligations.

Customer Reviews

4.9

20915 reviews

Ditto is doing really great. Absolutely spam free- that's the best part. They don't talk to you like they are forced to sell the product. It's more like, helping us buy better. Advisor Nuha was very patient and answered all my questions with clarity. Thanks for the service

I

INDHUMATHI M

Loved the service! Maheta Nidhi Hitesh was incredibly helpful and knowledgeable. She guided me through the whole process and made everything super easy to understand. I really appreciated how patient she was with all my questions—there was no pressure at all, just clear and honest advice. Honestly, I'm very happy with my experience at Ditto so far. Highly recommend!

RK

Ragul Kumar

I had a great experience with Ditto while exploring health insurance options. The process was smooth and everything was explained clearly.

A special thanks to Swaroop SK for patiently answering all my questions and guiding me through the policy details without any pressure. The transparency and support made it much easier to understand and choose the right plan.

Really appreciate the assistance!

PS

Pulkit Singh

Had a great experience with Ditto Insurance. Ishita Sudrania was extremely helpful in guiding me through choosing the right term plan. There was no spamming or sales pressure, and all my questions were patiently answered. She also assisted me thoroughly with the entire application process. Highly recommend!

SS

Samil Shah

I had a great experience with Ditto while filing my health insurance claim. Their team guided me clearly through the entire process, helped with the required documents, and promptly answered all my queries. Their support made the claim process much smoother and less stressful. Highly appreciate their assistance.