When selecting a term insurance plan, most people consider premium costs, sum assured, policy features, claim settlement record, and complaint volume, which is understandable. However, one important factor is frequently overlooked: the solvency ratio in term insurance.

In this article, we break down what the solvency ratio of insurance companies means, how IRDAI regulates it, and which insurers consistently maintain strong term insurance solvency ratios.

What is the Solvency Ratio in Term Insurance?

The solvency ratio in term insurance reflects an insurer’s financial stability. It indicates that the company has enough capital reserves to handle multiple claims, especially during high-claim events such as pandemics or natural disasters.

How to Calculate the Solvency Ratio?

The ratio is calculated by comparing the insurer's available capital to the risk it has taken on.

Solvency Ratio = (Available Solvency Margin) / (Required Solvency Margin)

- Available Solvency Margin (ASM): The amount of money remaining after an insurance company has paid all its liabilities. It acts as a safety net, helping the insurer handle unforeseen or higher-than-expected claims.

- Required Solvency Margin (RSM): The minimum level of capital that IRDAI requires an insurer to maintain, based on the risk exposure of its policies. It must be at least 50% of the minimum capital specified under Section 6 of the Insurance Act, 1938. RSM is determined by the insurer's risk profile and represents the minimum capital required to ensure the company's financial stability.

Note: For life insurers, solvency calculations primarily account for long term risks such as mortality and liabilities associated with long-duration policies.

Importance of Solvency Ratio in Term Insurance

Term insurance policies last 30–40 years and offer large payouts, so insurers must remain financially stable. The solvency ratio shows that the company is not just relying on premium income but has sufficient capital reserves to meet future claims. A low solvency ratio may result in delayed claim settlements, disputes, or difficulties during periods of high claim volume, and in extreme cases, insolvency.

IRDAI Guidelines on Solvency Ratio of Insurance Companies

IRDAI enforces stringent solvency regulations to safeguard policyholders and guarantee insurers' continued financial stability.

- Minimum Requirement: Insurers must maintain a solvency ratio of at least 1.5x to demonstrate adequate financial strength.

- Regular Monitoring: Companies are required to report their solvency position to IRDAI every quarter to ensure ongoing compliance.

What Happens If the Solvency Ratio Falls Below the Required Level?

Real-World Example: In 2023, the Insurance Regulatory and Development Authority of India (IRDAI) directed the transfer of the entire life insurance portfolio of Sahara India Life Insurance Company Ltd. to SBI Life Insurance. The decision was taken after Sahara Life faced prolonged financial and governance challenges. As a result, nearly 2 lakh policies were moved to SBI Life to ensure continued protection and servicing of their policies.

How to Check Solvency Ratios of Insurance Companies?

IRDAI Annual Reports

The Insurance Regulatory and Development Authority of India publishes solvency data for insurers in its annual reports, which are available on the regulator’s official website.

Insurer’s Public Disclosure Section

Most insurance companies publish their solvency ratio and financial details in the public disclosure section of their websites.

Form L-32 (for Life Insurers)

If you want to check the solvency ratio of life insurance companies, refer to Form L-32 in their public disclosure documents.

Ideal Solvency Ratio for Term Insurance Buyers

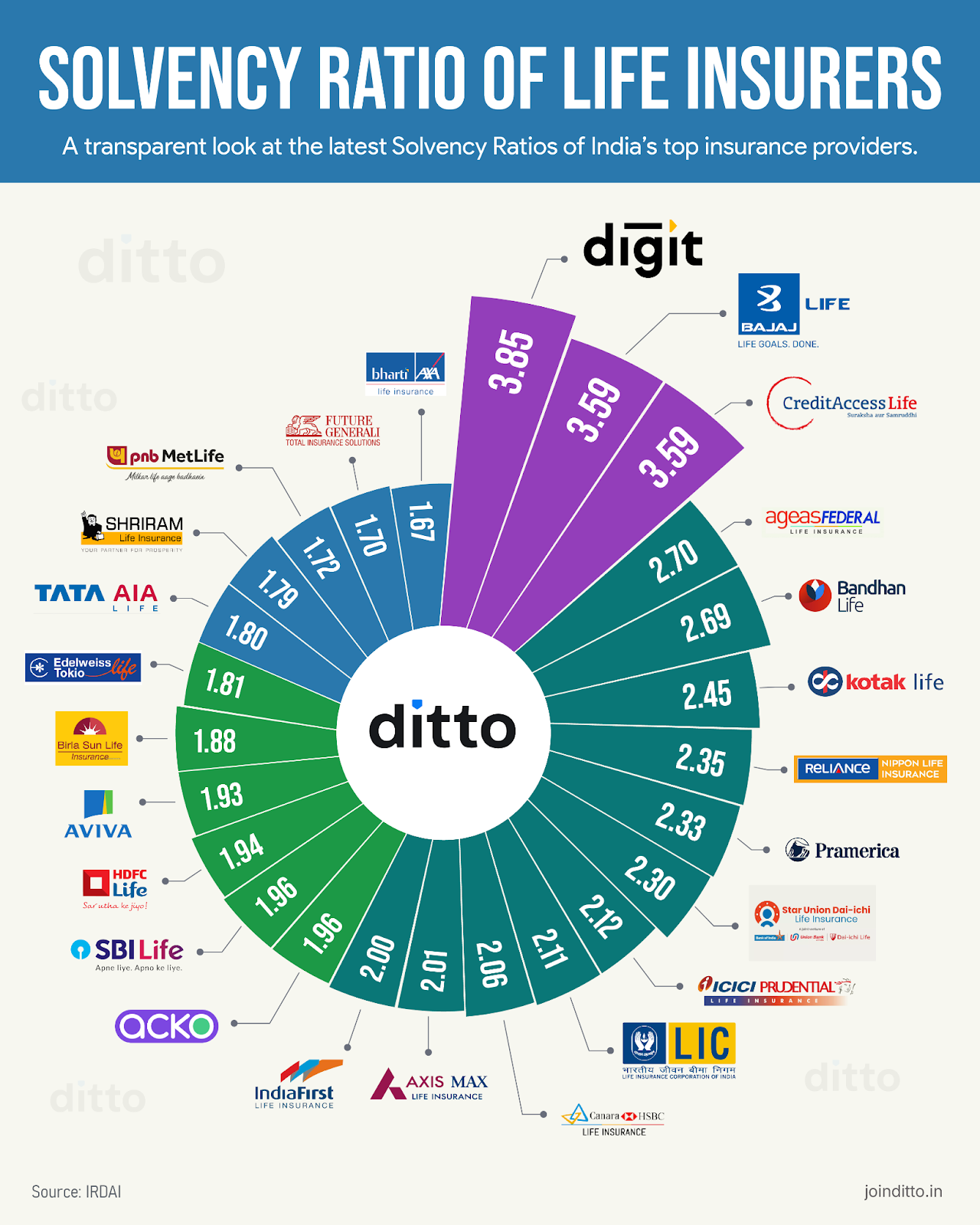

In general, the higher the solvency ratio, the better, as it reflects stronger financial reserves. While the regulatory minimum is 1.5x, the industry median is around 2.04x. Insurers above this level are generally considered financially strong. The solvency ratio applies to the life insurer as a whole and not just its term insurance business.

However, the solvency ratio in term insurance should be evaluated alongside other metrics, such as the claim settlement ratio (CSR) and the amount settlement ratio (ASR). You must also review annual business volume, complaints per 10,000 claims, overall policy performance, and customer experience. At Ditto, we recommend considering a three-year average of performance metrics for more consistent insights, instead of focusing on just one year.

Here are the solvency ratios of major term (life) insurers in India for FY 2024–25, as per the latest IRDAI Annual Report.

Top 5 Term Insurance Companies by Solvency Ratio

Curious about other metrics published by insurers and IRDAI? Ditto Data Lab gives you access to term insurance data that has been researched, organised, and curated by our team.

Note: The data in the above tables are sourced from the official IRDAI annual reports. For the most recent solvency ratio, refer to the insurer’s latest public disclosure filing. While IRDAI reports allow standardized annual comparisons, insurer disclosures are usually more up-to-date.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

You can book a FREE consultation. Slots are running out, so make sure you book a call now or chat on WhatsApp now!

Conclusion

The solvency ratio in term insurance is a key indicator of an insurer’s financial strength and ability to meet future claims. However, a very high ratio alone doesn’t provide the full picture. It may indicate that the company is holding excess capital instead of using it efficiently to settle claims or expand its business.

The ideal insurer maintains a solvency ratio well above 1.5x, with a strong claim settlement record, low complaints, and solid performance across key metrics. It is safer to choose insurers that maintain higher solvency ratios consistently over several years.

Disclaimer: This information is for educational purposes only. Please consult a licensed advisor before making any insurance decisions.

Frequently Asked Questions

Last updated on: