Term insurance plans are considered pure financial protection tools. They are designed to act as your financial replacement in the event of your unfortunate absence and help your family achieve their lifestyle goals without any financial compromises. Considering the substantial amount involved, potential policyholders are correct in prioritising the choice of their insurance provider and thus often fall back on famous and well-known brands with extensive insurance track records, like SBI Life.

However, term insurance policies gained popularity across the industry, considering their flexibility and customisation (over riders), affordability (cheaper premiums), and high coverage. Now, when it comes to age-old insurers, offering such comprehensive policies and keeping the policies updated with features and riders that cater to the recent financial goals of Gen X and the millennials might be a bit difficult. Subsequently, such term insurance policies from evergreen stables, like SBI Life, aren’t usually the preferred choice.

Now, coming to the SBI Life eShield Plan, we wonder if its features, riders, and premiums would succeed in making it a good pick! Let’s explore and find out!

Quick Verdict on SBI Life eShield Plan

SBI Life eShield Plan: Brief Overview

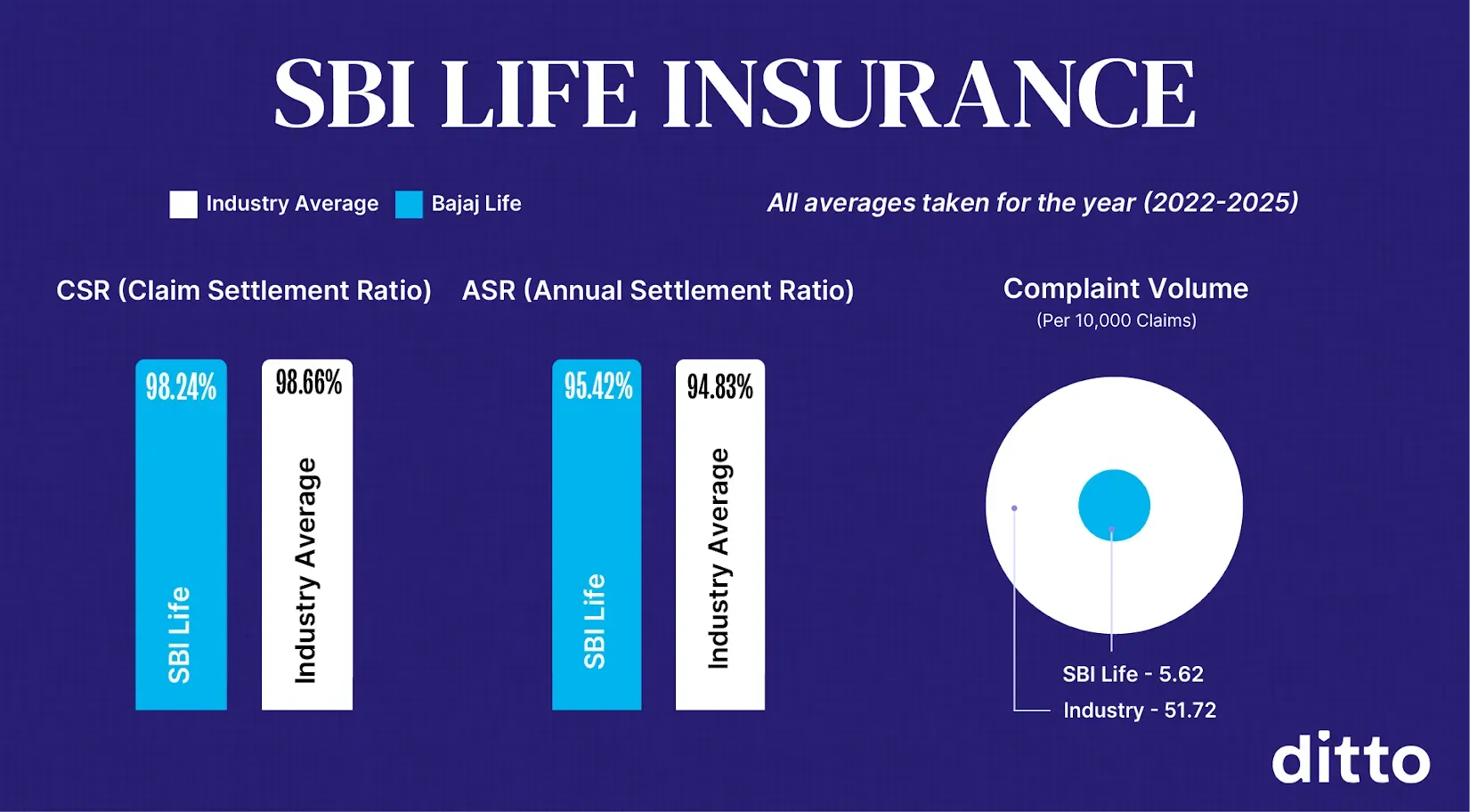

SBI Life commenced operations in 2000 as a joint venture between the State Bank of India (SBI) and French financial institution BNP Paribas Cardif. The insurer’s brand equity earned it a well-founded reputation as a life insurer, offering a diverse range of financial products, including life insurance policies, insurance plans with wealth creation, retirement plans, and more. The credibility of the insurer is also well established as per the metrics data (average of the last 3 years) mentioned below -

- Claim Settlement Ratio (CSR) of 98.24% (the industry average is 98.66%)

- Amount Settlement Ratio (ASR) of 95.42% (the industry average is 94.83%)

- Complaint Volume of 5.62 (the industry average is 51.72)

Despite its great credentials and brand backup from one of the largest public sector banks (SBI) in India, the company has yet to launch a comprehensive and affordable line of life insurance products. Much of this obstacle can be attributed to the missing riders and features in its term insurance policies that are otherwise readily available in the best term plans in the market. Additionally, plans from this stable tend to be a bit pricier than the rest in its category.

Coming to the SBI Life eShield Plan - this is not much of a recommended plan, primarily because of its diverse restrictions, limited coverage, few riders, and more. For starters, in the case of smokers, the plan's maximum coverage is capped at ₹99 lakhs only. So, in case you are a smoker, you need to consider whether this ₹99 lakhs is sufficient as your income replacement.

Again, the plan offers only a few riders - Accidental Death Benefit and Total and Permanent Disability Rider. The plan has 3 options - Level Cover, Increasing Cover, and Level Cover with Future Proofing Benefits based on the presence or absence of an in-built perk of increasing cover (based on inflation or life stages).

It is pretty obvious why we wouldn’t usually recommend this plan to you unless you specifically ask for it or are an SBI brand loyalist (because this plan doesn’t offer all of these features either as an in-built perk or as an add-on). In case it’s the latter and you are interested in the SBI Life eShield Plan, here is a quick look at its features -

SBI Life eShield Plan: Table of Features

Should You Buy SBI Life eShield Plan?

- SBI as an insurer: SBI Life has a sizeable share of insurance policyholders, thanks to the brand identity provided by the SBI Bank. However, despite the brand's credibility and great data metrics across CSR, ASR, and Complaint Volume, it is undeniable that this is a public sector-owned insurance provider. Naturally, there are multiple restrictions across the features in the term insurance plans offered by this stable, making them non-comprehensive.

Now, considering that term insurance policyholders have convenient access to credible insurers offering value-worthy and affordable feature-rich policies, SBI Life’s life insurance products lose the much-required edge.

2. In-built features of the plan: The SBI Life eShield Plan is not a comprehensive policy and might not be a good pick. The in-built features are pretty limited. Here’s a look at its built-in features -

a. Eligibility-based coverage: Now, it’s true that term insurance providers are stringent about considering the annual income of potential policyholders as an eligibility factor when deciding if they can extend a policy at all and the sum assured capping that can be offered.

However, in the case of the SBI Life eShield Plan, the financial restrictions are a bit more limiting - if you are a smoker, your upper limit for coverage is ₹99 lakhs. Such limited overage might not suffice (consider inflation, any loans you have availed, and the life stage goals of your dependents) as a future income replacement for you.

b. Death Benefit: Much like any of the standard term insurance plans in the market, the SBI Life eShield Plan offers a death benefit to the beneficiary if the policyholder passes away during the policy tenure. This death benefit perk has 3 options based on whether you choose to increase the cover in terms of inflation or life stage requirements -

- Level Cover: In this case, the insurer offers you the base sum assured that remains fixed from the day you purchase the policy till the death of the policyholder.

- Increasing Cover: In the case of the Increasing Cover option, the base sum assured (chosen at the time of policy purchase) increases by 10% every 5 years during the policy year (till the base sum assured doubles) or till the policyholder reaches 71 years old - whichever comes earlier. This is in sync with the inflation rate.

- Level Cover with Future Proofing Benefits: In case of this option, the base sum assured can be boosted during significant life stage events like - marriage (by 50% of the base sum assured, up to ₹50 lakhs), birth/adoption of 1st and 2nd child (by 25% of the base sum assured, up to ₹25 lakhs), and home loan (up to ₹50 lakhs or the home loan amount, whichever is lower - this can be availed only once during the policy tenure).

c. Terminal Illness Benefit: Say you have been diagnosed with a terminal ailment, and your doctor gives a written declaration that you have a poor prognosis with only a few months to live. Once you produce this information to the insurer, your insurer under the SBI Life eShield Plan will offer you a Terminal Illness Benefit of up to ₹2 crores. The maximum terminal illness is capped at the sum equal to your cover amount.

If your terminal illness is less than the cover amount, the residual amount is provided to the beneficiary when the policyholder passes away.

Remember, this perk kicks in only if the terminal illness diagnosis is made/the policyholder dies within the policy tenure or before the spouse turns 80.

3. Available Riders:

- Accidental Death Benefit: If the policyholder passes away due to an accident within 120 days of the accident, the insurer offers an additional lump sum amount of up to ₹50 lakhs or the base sum assured (whichever is lower). This amount is over and above the base cover amount.

- Total and Permanent Disability Rider: If the policyholder is left totally and permanently disabled following an accident, the insurer offers up to ₹50 lakhs as a lump sum or in instalments to be used as an income replacement, considering the disability might lead to a compromised source of income.

- Better Half Benefit: Under this SBI Life eShield Plan rider, the policyholder and their spouse are covered. Say, if the primary policyholder passes away or has a terminal illness diagnosis, the spouse receives ₹25 lakhs as a lump sum in the mode of a Level Cover. Even if the primary policyholder passes away, the policy stays intact till its maturity age(as chosen during policy purchase). However, this perk can kick in only if the policyholder passes away before the spouse reaches 60.

What’s Unique About the SBI Life eShield Plan?

Unfortunately, the SBI Life eShield Plan doesn’t have many unique features. It has 3 plan options, a few riders (Better Half Benefit, Accidental Death Benefit, and Total and Permanent Disability Rider), and a few in-built features. However, the policy has a few restrictions based on income and smoking habits that limit the perks substantially.

Why Choose Ditto for Term Insurance?

At Ditto, we’ve assisted over 8,00,000 customers with choosing the right insurance policy. Why customers like Vijay below love us:

- No-Spam & No Salesmen

- Rated 4.9/5 on Google Reviews by 15,000+ happy customers

- Backed by Zerodha

- Dedicated Claim Support Team

- 100% Free Consultation

Confused about the right term insurance? Speak to Ditto’s certified advisors for free, unbiased guidance. Book your call or WhatsApp us now, slots fill up fast!

Conclusion

To conclude, the SBI Life eShield Plan fails to meet our expectations. The restriction on coverage (for smokers and based on income eligibility), along with offering only a few riders, makes it a non-comprehensive policy that is pricier than it is worth. Additionally, the absence of features like life stage perks (available only in 1 plan option), critical illness benefits, and waiver of premium - make it a tailender in our list of recommendations for the best term insurance plans. We would love for you to consider and compare the best term plans and choose one from there.

Last updated on: